Liquidity flows where confidence sits. And right now, JPMorgan is positioning itself at that intersection – reshaping how digital dollars are built, regulated, and deployed at scale.

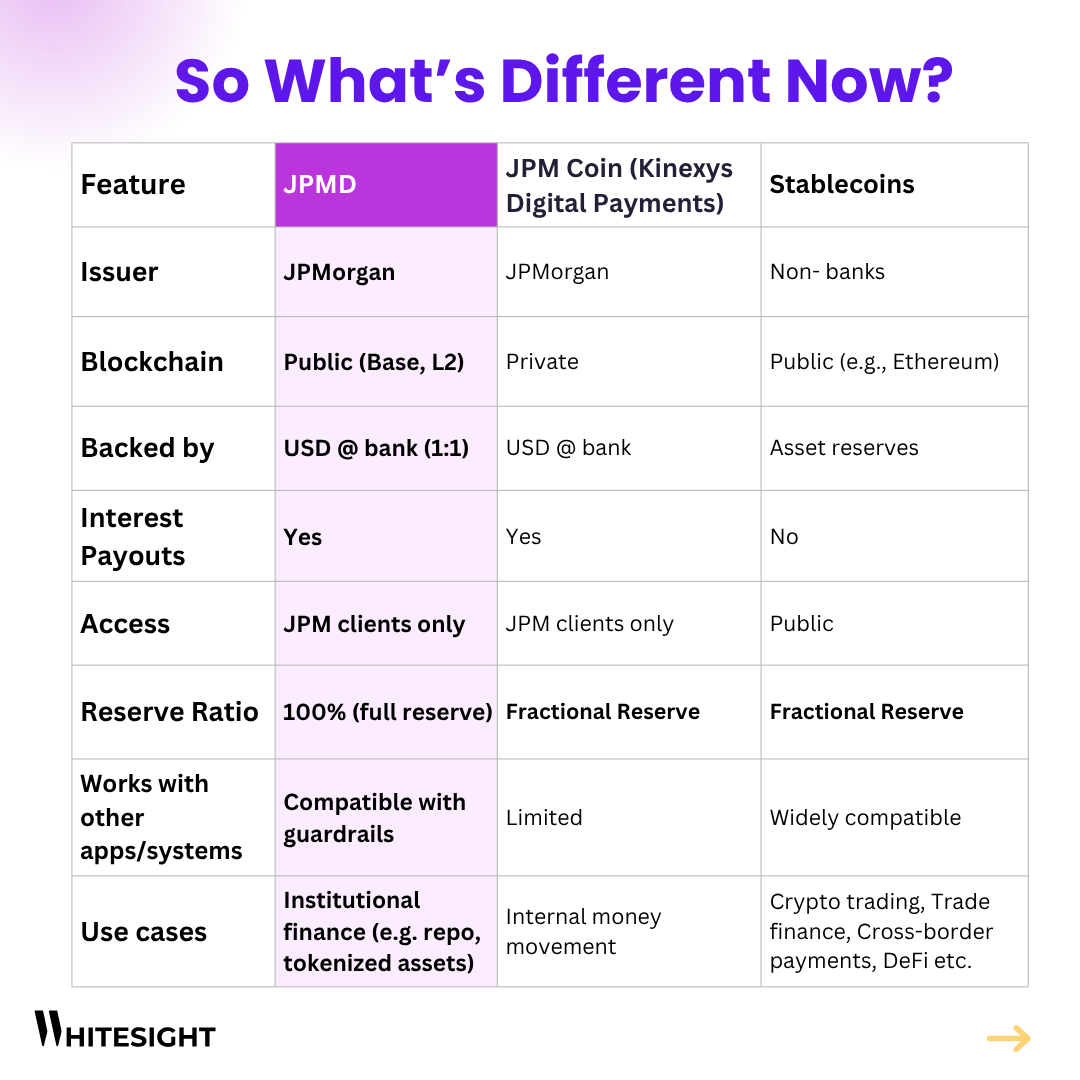

The launch of JPMD, a tokenized bank deposit issued on Base (an Ethereum Layer 2), signals more than an infrastructure upgrade. It marks a strategic shift. For institutions that have watched the crypto world from a cautious distance, this is not a tentative test. It’s a full step into programmable money, done on public rails, under the rules of traditional banking.

Stablecoins are not being sidelined in this story. If anything, they set the tone. JPMD learns from their speed, their flexibility, and their composability. But it doesn’t stop there. It builds in the regulatory muscle, governance logic, and operational guardrails that banks need, not just to experiment, but to transact with intent.

What JPMD is, and why the structure matters

How private rails set the foundation:

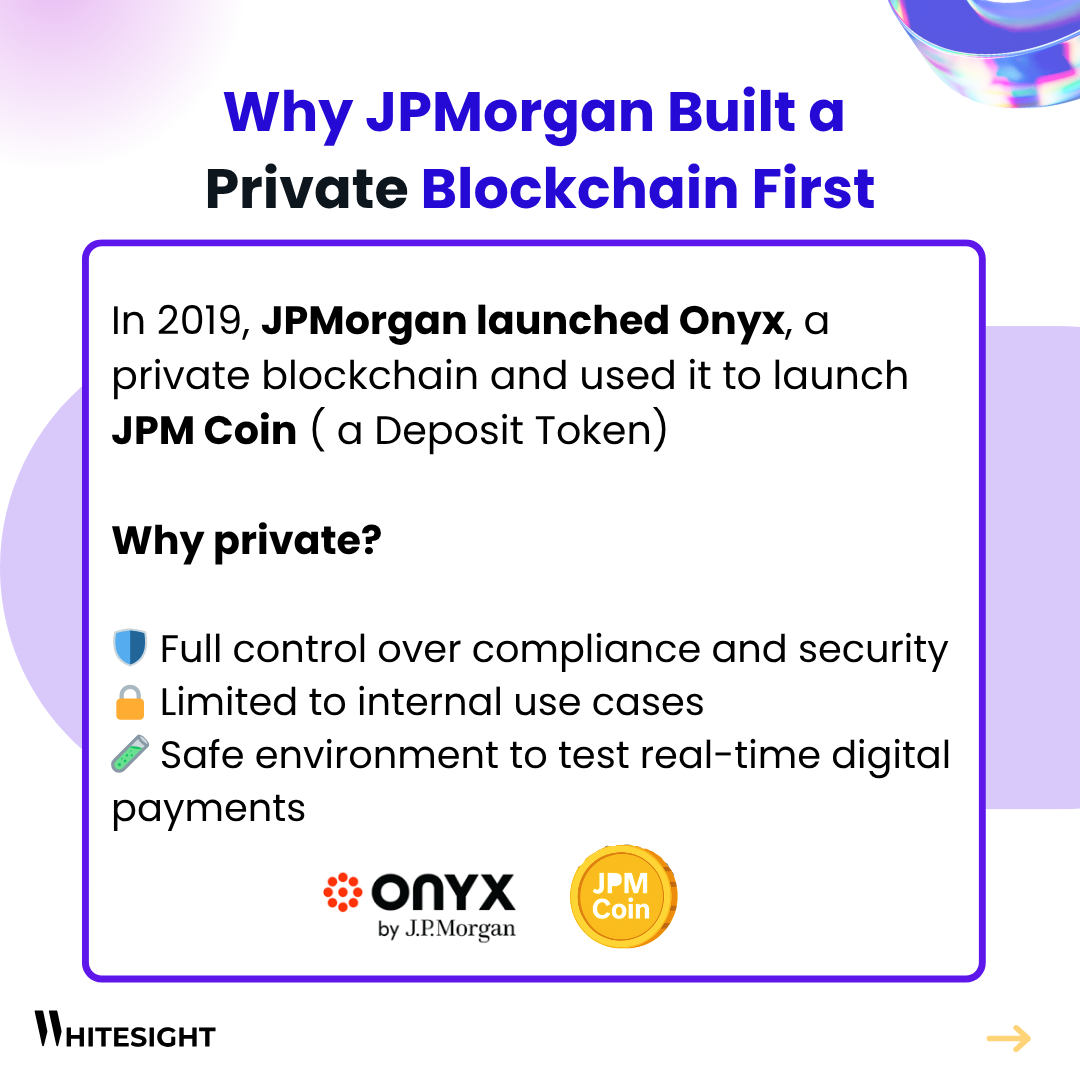

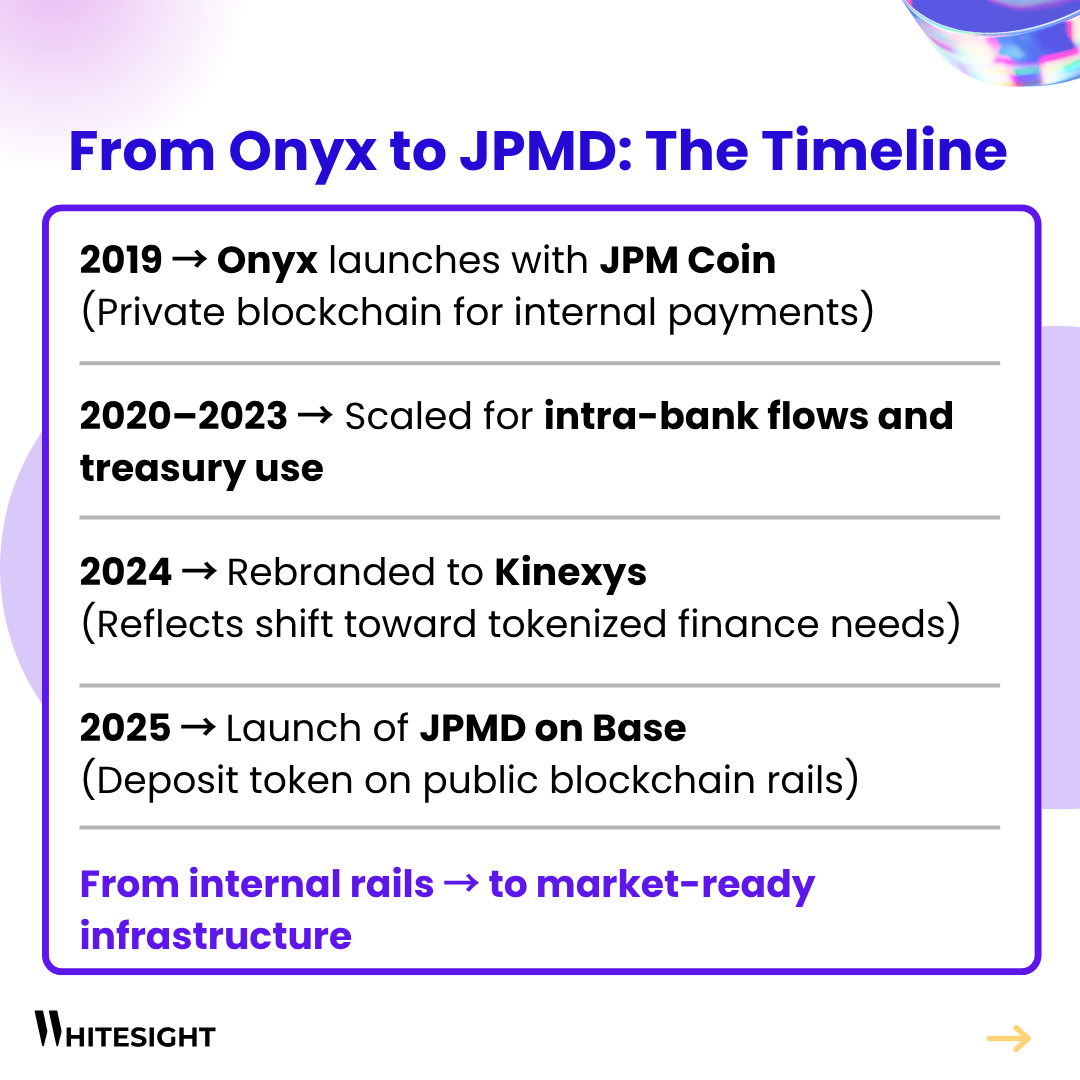

JPMorgan didn’t get here overnight. In 2019, it launched Onyx, a private blockchain designed to support internal operations, including liquidity corridors, treasury flows, and inter-entity settlements. Within that environment, the bank introduced JPM Coin, a digitised deposit token used for moving funds across entities faster than traditional rails allowed.

Onyx proved valuable for closed-loop use cases, but as tokenized assets matured outside its walls – money market funds, repo agreements, FX – the limitations became clear. By 2024, it was time to expand.

That’s when Onyx was rebranded to Kinexys, a move that signalled a shift from controlled networks to market-facing platforms. And JPM Coin itself was repositioned as Kinexys Digital Payments, with a broader mandate to enable asset-backed flows across connected platforms.

JPMD now sits as a separate product – purpose-built to work in public blockchain environments, but with safeguards that align with how institutions operate.

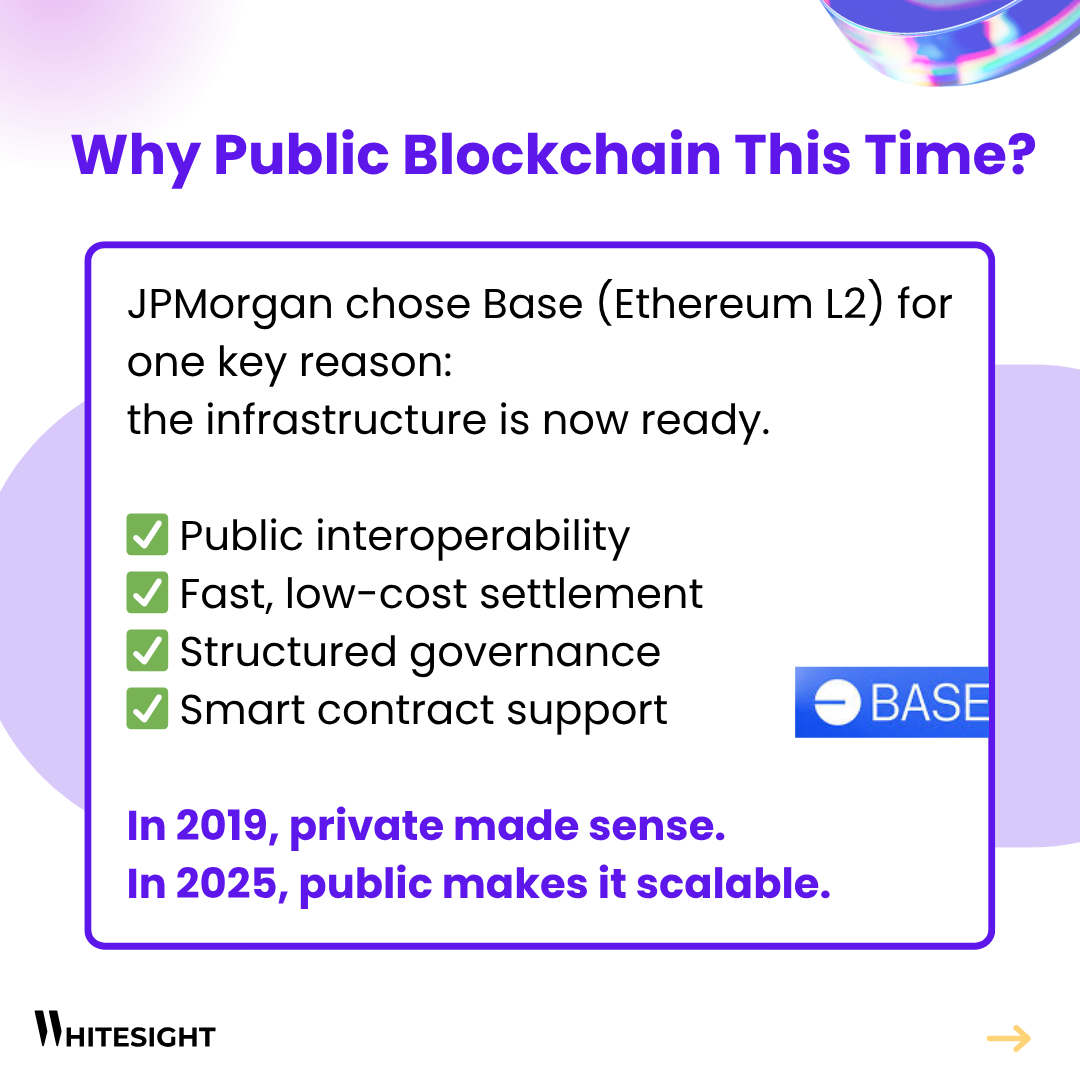

Why Base, and why this matters now:

Base, Coinbase’s Layer 2 network built on Ethereum, offers a balance that makes sense for JPMorgan. It delivers lower fees, faster throughput, and compatibility with Ethereum tooling. More importantly, it supports permissioned environments on top of public infrastructure – a design that mirrors what banks need.

For JPMD, this means it can operate where tokenized assets live, without losing the protections expected by regulators and institutions. This alignment becomes crucial when the intent is not experimentation, but daily settlement, collateral movement, and capital efficiency at scale.

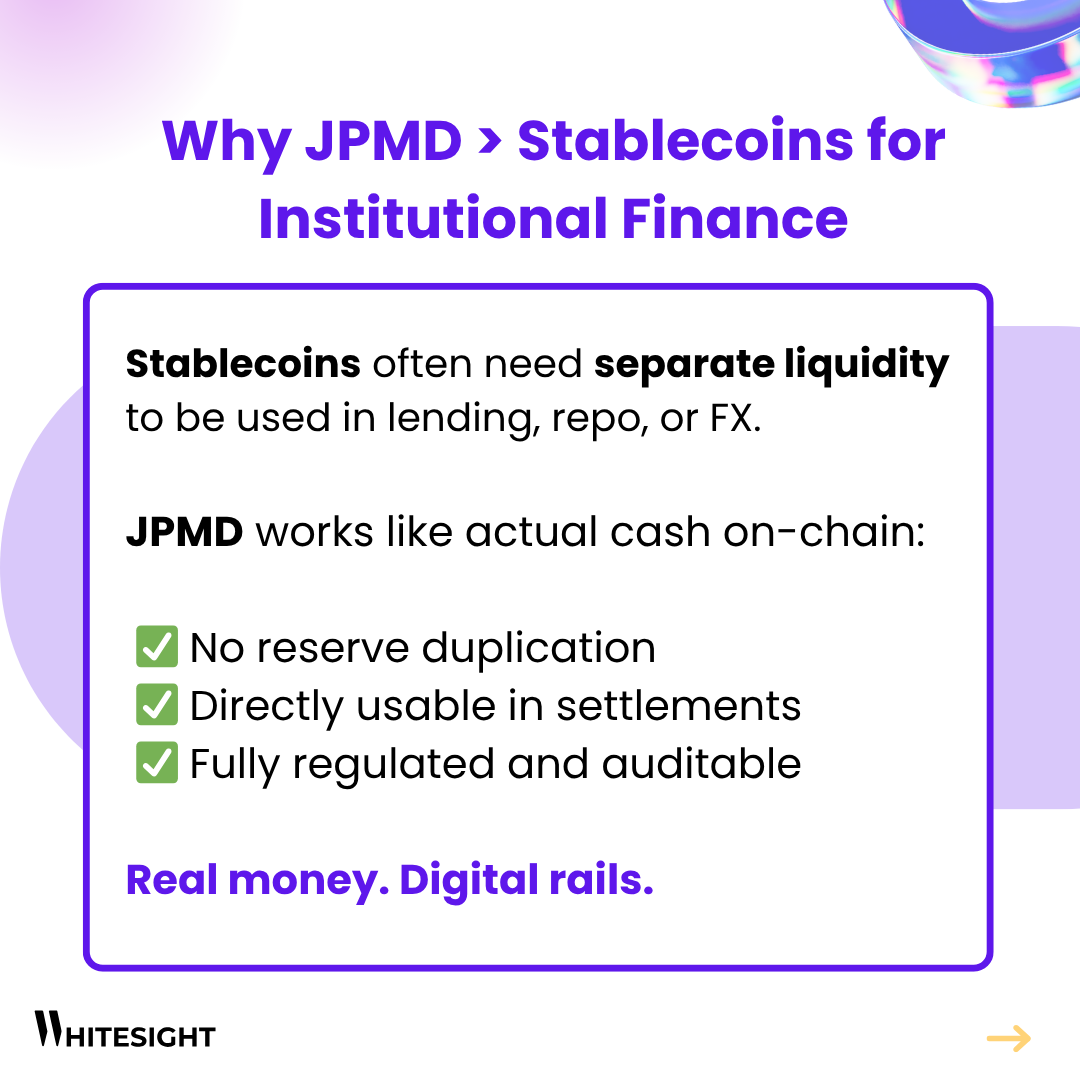

Stablecoins showed demand – JPMD targets structure

Stablecoins deserve credit for proving that people want dollars on-chain. They enabled high-frequency trading, global remittance flows, and basic interoperability between crypto platforms. But they weren’t built for regulatory certainty.

Many are backed by reserves that fluctuate in composition. Others operate under loosely defined legal frameworks, or depend on infrastructure that exists outside the scope of traditional oversight. For institutions, that creates friction. It means lawyers, workarounds, and operational disclaimers.

JPMD answers those frictions. It brings the benefits of tokenized money – speed, programmability, compatibility – into a format that works for institutional workflows. You don’t have to build around it. You can build with it.

What this really signals:

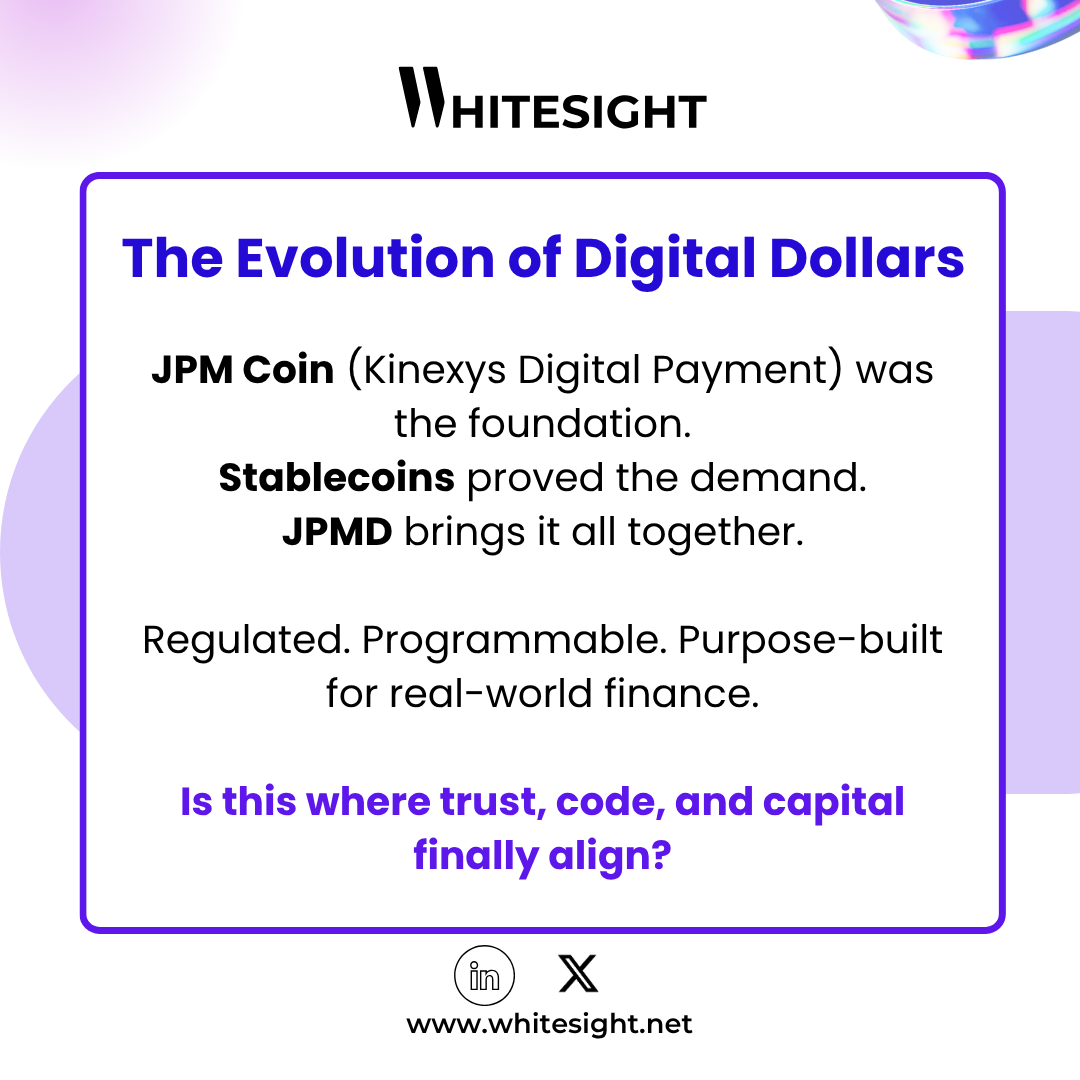

JPM Coin proved that digital cash could work inside the bank. Stablecoins proved that programmable dollars could move across the internet. JPMD brings those ideas together in a format that meets the standards of financial institutions, not as an experiment, but as a tool meant for production.

If more banks follow this path, the real questions won’t be about token design or blockchain compatibility. They’ll be about who defines settlement logic. Who controls the rails? And which infrastructures quietly become default, not because they shouted the loudest, but because they functioned best at scale. JPMorgan is not waiting to find out. It’s building with that future in mind.

Our monthly Digital Assets newsletter unpacks the latest across stablecoins, tokenization, crypto trading, and global regulations, all in one punchy read. Perfect for staying ahead of the curve without the scroll fatigue.

Read the latest issue and subscribe to catch the next drop this week!

Unlock the deep dives into the winning strategies of Stripe, Apple, Starling Bank, and more with a WhiteSight Radar Membership.

Join 4,000+ fintech buffs already subscribed and get unparalleled access to expert reports, industry trend breakdowns, and exclusive insights on everything from Embedded Finance to Digital Banking, Open Finance and beyond—all at a fraction of the cost of market alternatives.

Supercharge your Fintech IQ with WhiteSight Radar, putting expert fintech intel at your fingertips! You’ll be joining a growing global community of fintech professionals. 🧭

Actionable insights on fintech, delivered regularly. Join Radar for exclusive fintech content and member benefits.

Be the First to Know About the Next Big Fintech Strategies!

We’ve got a power-packed lineup of strategy playbooks coming soon—including Nubank, Affirm, Wise, and more. With 1,000+ report downloads and 100+ paid subscribers, we’re the go-to for fintech intelligence.

Want to be the first to access every new report, blog, and market insight as soon as it drops?

Subscribe to receive our updates directly in your inbox!

Don’t miss out on the next big fintech wave! Follow us on LinkedIn for daily updates and in-depth analysis. Subscribe to our weekly newsletter for curated insights delivered straight to your inbox. Unlock exclusive access to our membership plans for deeper dives into market trends, competitor analysis, and investment opportunities.

Login to access Fintech intelligence

Sign up to access Fintech intelligence