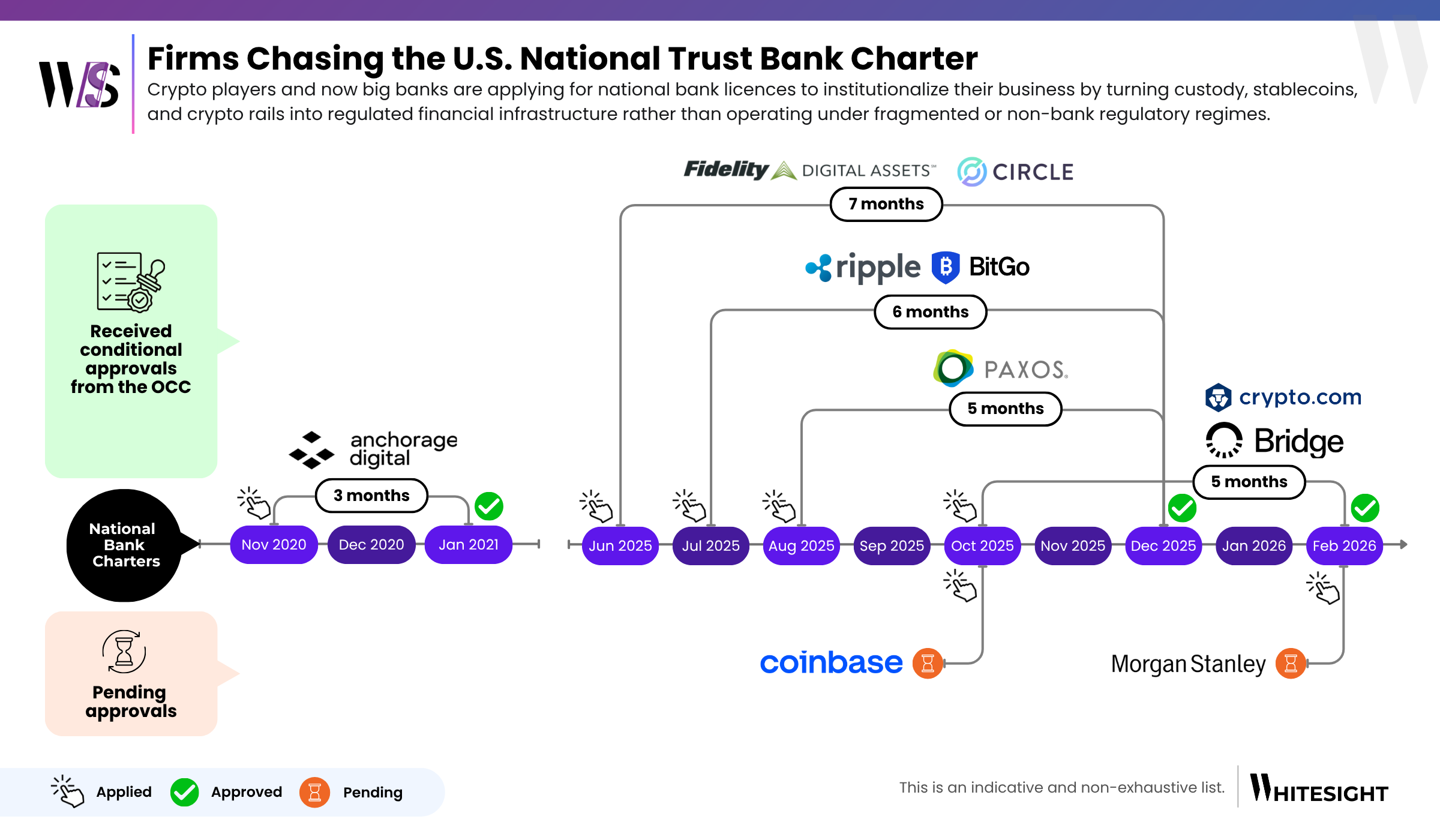

The OCC trust-bank route is becoming an important pathway for companies building around stablecoins, custody, and digital asset settlement. Bridge, now a Stripe company, showed why payments companies want an OCC-supervised structure around stablecoin custody and reserves. Crypto.com’s conditional approval for a national trust bank charter points to the same pull from the exchange side.

The trend is no longer limited to crypto-native firms, with larger financial institutions also exploring trust-bank licences as digital asset activity moves closer to regulated financial infrastructure.

Stablecoins already function as a faster settlement rail. The bigger challenge has been institutional adoption at scale. Large platforms, treasuries, and financial institutions need clear answers before moving meaningful volume: who is the regulated entity, where the assets sit, what controls exist, and who examines the structure.

A national trust-bank setup helps answer those questions. It gives crypto firms, payments companies, and custodians a recognised regulatory wrapper that can make institutional participation easier. The companies that secure these licences may be better positioned to support stablecoin use cases at scale because they reduce uncertainty around custody, reserves, governance, and supervision.

The impact is practical. Approvals can move faster when compliance teams can anchor on a known supervisor. Transaction limits can move higher when governance, controls, and reporting are easier to defend. That is why exchanges, issuers, custodians, and payment companies are moving toward the same structure: each wants to become the trusted counterparty when stablecoin pilots turn into production deployments.

This also pushes the market toward a more concentrated structure. Fewer providers may be selected, and partnerships will matter more. Companies without a trust-bank wrapper may need to integrate with those that have one. The prize is becoming the trusted gateway for stablecoin settlement across payouts, cross-border payments, and treasury flows.

It is also important to separate this from full-service banking. National trust banks do not take deposits and do not come with FDIC insurance. This is not about becoming a traditional bank. It is about control, custody, supervision, and credibility.

Actionable insights on fintech, delivered regularly. Join Radar for exclusive fintech content and member benefits.

Don’t miss out on the next big fintech wave! Follow us on LinkedIn and subscribe to our Future of Fintech Newsletter to be the first to know about the Next Big Fintech Strategies.

Don’t miss out on the next big fintech wave! Follow us on LinkedIn for daily updates and in-depth analysis. Subscribe to our weekly newsletter for curated insights delivered straight to your inbox. Unlock exclusive access to our membership plans for deeper dives into market trends, competitor analysis, and investment opportunities.

Login to access Fintech intelligence

Sign up to access Fintech intelligence