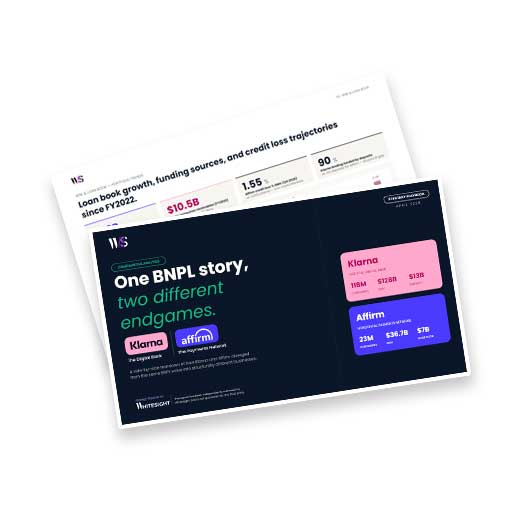

BNPL began with a simple proposition: make credit frictionless at checkout. While both Klarna and Affirm emerged from the same BNPL paradigm, their trajectories have fundamentally diverged into two distinct operational and economic models. This report examines the structural shift from simple credit provision to complex financial ecosystems, where the primary objective is no longer merely facilitating a transaction, but capturing the entirety of the consumer’s financial lifecycle. Klarna is moving toward a vertically integrated digital bank, using its banking licence, $13B deposit base, cards, wallet, and P2P payments to deepen the consumer relationship beyond purchase. Affirm, by contrast, is building toward a horizontal payments network, embedding installment intelligence across merchant checkouts, cards, wallets, issuer rails, and everyday payment moments.

Colombia’s banking sector is controlled by four incumbents holding three-quarters of all personal deposits. Savings accounts carry sub-1% yields. 65% of the population is locked out of formal credit and have to resort to informal street lenders at 382% APR because the formal system cannot serve them.Nu Colombia entered this market in September 2020 with a single credit card. By February 2026, it held the #1 net card issuer position every year since 2022, 5.75% of all savings deposits, and the second-largest CDT book for individuals, captured within six months of launching the product. At WhiteSight, we’ve deconstructed the full strategy behind this expansion, from the credit-first entry logic and the three-card architecture that tripled approval rates inside the usury ceiling, to the funding mechanics that systematically replaced expensive capital with the cheapest source available: retail deposits.

From its origins as a niche student loan refinancer to its valuation as a $33B diversified financial powerhouse, SoFi has transformed the boundaries of digital banking in the U.S.. By integrating consumer banking with a high-margin B2B technology layer through Galileo and Technisys, SoFi might just be building the AWS of Fintech. With a deposit engine reaching $37.5B, SoFi’s journey is a blueprint for how vertical integration can unlock long-term profitability and scale in a competitive landscape

Adyen has become the powerful financial infrastructure beneath some of the world’s largest platforms such as Uber, Etsy, eBay, Toast, Oracle, SAP. This report maps the full strategic playbook: from how Adyen evolved from a payments processor to a full-stack embedded finance enabler. By partnering with enterprise software platforms and SMB marketplaces, Adyen created an indirect distribution network that reaches enterprises, small businesses, and individuals at scale — at a fraction of what it costs traditional financial services players to acquire and serve those same segments.

Onchain finance is moving into the core of the financial system.Across 2025 and Q1 2026, Visa and Mastercard moved further into this space by becoming the integration layer. Visa extended its model across public blockchains, enabling stablecoin settlement, card issuance, wallet integrations, and cross-border flows through partners and APIs. Mastercard built its MTN network, where institutions join a permissioned environment to issue, transfer, and settle tokenized assets.The scale reflects this shift. Visa’s stablecoin settlement platform reached $3.5B in annualized volume across four blockchains and four stablecoins, and supports 130+ stablecoin card programs across 40+ countries. Mastercard acquired BVNK for $1.8B to bring stablecoin infrastructure into its network, while MTN expanded into EEMEA with participants including JPMorgan, Standard Chartered, and SoFi.

Australia is one of those markets that looks attractive from the outside and unforgiving in practice. Xinja folded. Volt shut down. 86 400 was absorbed. Yet Revolut, a UK challenger with no banking licence, crossed 1 million customers and turned profitable.

Most foreign digital banks that entered the US burned cash, hit the regulatory wall, and retreated. Nubank entered with a conditional OCC charter, $2.9B in net profit, and 4–5 million customers already active in the US. With 131 million customers across Latin America, the question is whether it has found the model that finally makes a foreign digital bank work at scale in America.

Most SME neobanks can win attention. Far fewer can attract deposits, build a meaningful loan book, and reach profitability. Allica has done all three. Now, with a fresh $155 million Series D and ambitions beyond the UK, the bigger question is whether it has found one of the few scalable models in SME banking.

Adyen was built to replace fragmented payment stacks with a single platform that handles payments end to end. That foundation has scaled to €1.4T in processed volume in 2025, with net revenue nearing €2.4B. By bringing online, in-store, and in-app payments into one platform, Adyen turns transactions into shared data that strengthens reporting and optimization across channels.At WhiteSight, we’ve unpacked Adyen’s growth strategy, highlighting the product and market moves driving this expansion.

Monzo went from challenger bank to a £1.2B-revenue machine, without losing its inimitable Hot Coral halo. What actually powered the step-up: Flex’s shift from BNPL to full-stack credit, paid plans with real stickiness, and SME monetisation at scale. Grab the deep dive for hard numbers, product moves, and the playbook behind 12.2M customers and counting.

From disrupting cross-border money movement to building a 60M+ customer base across 48 countries, Revolut has consistently stretched the boundaries of what a digital bank can be. Now, CEO Nik Storonsky has set a new ambition: to make Revolut the first truly global bank – serving 100M customers, in 100 countries, and generating $100B in revenues. With investors projecting a $242B valuation by 2030, Revolut’s journey is now about becoming An Everything Bank for Everyone.

At WhiteSight, we’ve unpacked the strategy behind this vision, uncovering how Revolut is shaping its model, products, and market moves to turn ambitious goals into a global reality.

BNPL shifted deeper into retail and banking infrastructure, while tokenisation gained serious ground in real estate and assets. Licensing activity heated up across the UAE, Saudi Arabia, and Egypt, reshaping virtual assets, digital wallets, and e-KYC. Meanwhile, fintechs are scaling across borders, tapping into high-demand markets and underserved segments with sharper models. WhiteSight’s latest report unpacks the moves, the capital, and the momentum that are setting the course for MENA’s fintech future.