Embedded Finance has existed in a loosely coupled manner for decades, where non-financial firms either partnered with financial firms or opened up financial arms as subsidiaries to serve the financial needs of customers and facilitate business transactions.

The current generation of embedded finance comes in a different flavour because it seamlessly integrates financial products into digital interfaces that consumers and businesses use frequently and smoothens the customers’ experience of availing financial services alongside non-financial services. For consumers, these digital interfaces could be e-commerce apps, ride-hailing apps, and social media platforms. For businesses, these may include accounting software, ERP systems and invoicing platforms. This makes it easier for consumers and businesses to access financial services as part of their regular personal or business activities.

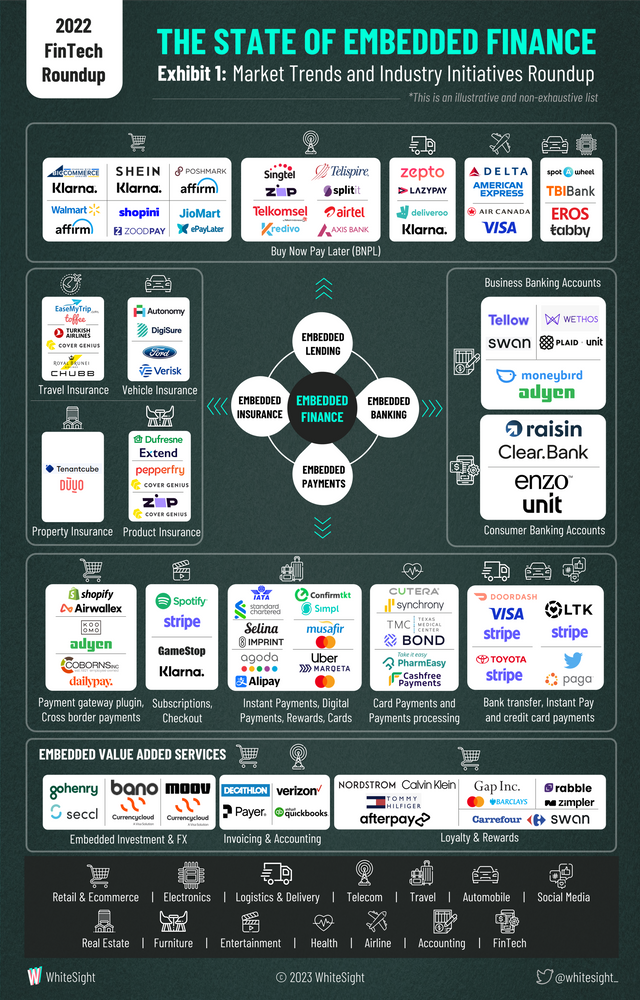

The embedded-finance product scope has expanded well beyond the payments and cards use cases to now include various types of bank accounts, credit products in the form of instalment loans and BNPL, investment offerings such as fractional investing and ISA accounts, and insurance coverage for health, vehicle and travel. Even complex products for businesses – such as forex, accounting and invoicing services – are also getting embedded into business platforms to unlock contextual experiences and efficient business operations.

Embedded Payments

Consumers and businesses are increasingly seeking convenient and seamless payment options, and this trend is driving the development of embedded payment solutions. For example, consumers may prefer to make payments using their mobile phone or another connected device rather than carrying a separate payment card or cash.

In 2022, notable developments included the payments platform Airwallex’s partnership with eCommerce giant Shopify for streamlined payments integration – embracing cross-border payments. On the other hand, payment giant Mastercard made waves in the travel industry as it partnered with online travel agent Musafir to digitise end-to-end payments for travel bookings from the Middle East and North Africa. It also collaborated with the ride-hailing app Uber, card issuing platform Marqeta and workforce payments platform Branch to power the Uber Pro Card.

Embedded Banking

Embedded banking refers to incorporating traditional banking tools such as debit cards and checking accounts into non-financial platforms like a marketplace or retailer. With embedded banking, non-financial firms offer their users a branded checking account to hold funds and make payments for consumers, freelancers, or businesses. Embedded banking offers multiple categories of accounts, such as “For Benefit Of” (FBO) accounts, stored value accounts, direct deposit accounts, etc.

For Business Banking clients, it also means a seamless experience where a business’ back-end systems are connected to their banks behind the scenes. This means the business owners or their treasury teams can manage accounting invoicing, payments and banking services seamlessly from one system that orchestrates the whole banking experience.

In 2022, several embedded banking initiatives were witnessed for freelancing, accounting and bookkeeping platforms.

Embedded Lending

Embedded lending refers to credit products that are integrated into other products or services rather than being sold separately. Companies are using technology, such as real-time data collection and machine learning, to improve underwriting efficiency and reduce fraud risk while offering embedded credit and BNPL products.

In 2022, BNPL services expanded extensively into industries like e-commerce, telecom, airlines and more. Retail giant Walmart and SaaS e-commerce platform BigCommerce were seen joining forces with leading BNPL service providers Affirm and Klarna, respectively, to offer flexible payment options. While telecom players such as Singtel collaborated with BNPL fintech Zip to launch its Pay Later service in Singapore, the airline industry saw Air Canada partnering with payment giant Visa to bring its BNPL Installment Solution to eligible credit cardholders. Other industries, such as logistics & delivery, automobiles and electronics, too, witnessed developments adopting flexible payment options.

Embedded Insurance

Embedded insurance refers to the integration of insurance protection into everyday products and services, making it easier and more convenient for people to access and use insurance. For example, a car manufacturer might offer an insurance policy that covers maintenance and repairs as part of the purchase price of a new car, or a retailer might offer accidental damage coverage as an add-on to the purchase of a new electronic device.

In the travel insurance space, Cover Genius collaborated with Turkish Airlines to provide their global passengers with comprehensive travel protection directly through Cover Genius’ XCover platform. Further, recognising the growing phenomenon of vehicle insurance, Ford joined Verisk Data Exchange, allowing eligible Ford and Lincoln owners to enrol in insurance programs that are also integrated into the exchange. Insurance companies can utilise Ford data with Verisk Driving Score to determine premiums based on driver behaviour data.

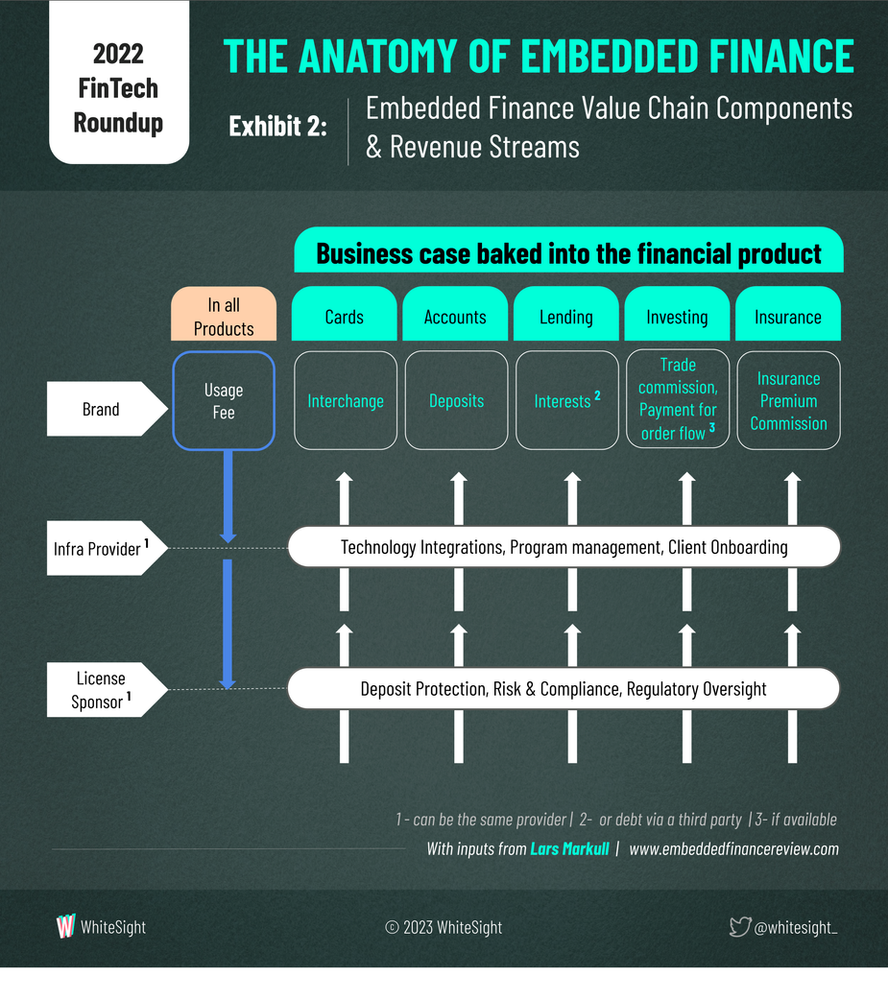

The Anatomy of Embedded Finance

There are many different motivations for embedding financial products into a non-financial offering. An increase in usage, lock-in effects and reduced churn from the main service is often a core element of such a decision towards embedded finance. Additionally, almost all financial products include an element that allows the non-financial brand to directly or indirectly monetise the financial offering.

The mechanism through which embedded finance gets orchestrated and delivered to end customers involves close collaboration with multiple participants and technology providers. Still, there’s always at least one chartered financial institution involved. The licensed financial firm could be in the form of a bank, a lending institution, a broker-dealer firm, or an insurance underwriter. At times the licensed firm chooses to use its own resources, i.e., balance sheet, technology, and business processes, to enable embedded finance experiences. Other times the licensed firm partners with third-party BaaS technology providers to orchestrate and distribute embedded finance experiences to brands. This involves a complex relationship in terms of process orchestration and revenue sharing among the value chain participants, as depicted in Exhibit 2.

The Road Ahead for Embedded Finance

Against the current volatile financial backdrop, embedded finance could be the hub for more innovative disruptors. Financial institutions, BaaS technology providers and companies from all sectors still have time to seize a piece of this dynamic industry. While the opportunity is significant and the technology pieces seem to be ready, the sector may witness heightened regulatory scrutiny as regulators have begun to take note of rapid participation from non-financial firms and Big Tech companies in the financial industry. With the slowdown forecasts, 2023 could emerge as a pivotal year when firms would find themselves at the crossroads to actively leverage massive opportunities of embedded finance and cautiously mitigate the firm-level risks and shadow banking risks that it entails for the financial sector.

Sanjeev is a fintech aficionado who loves to explore the depths of the industry as much as he loves to explore the depths of the ocean in his scuba gear. He is the founder and CEO at WhiteSight, bringing a wealth of research and advisory experience to the fintech world.