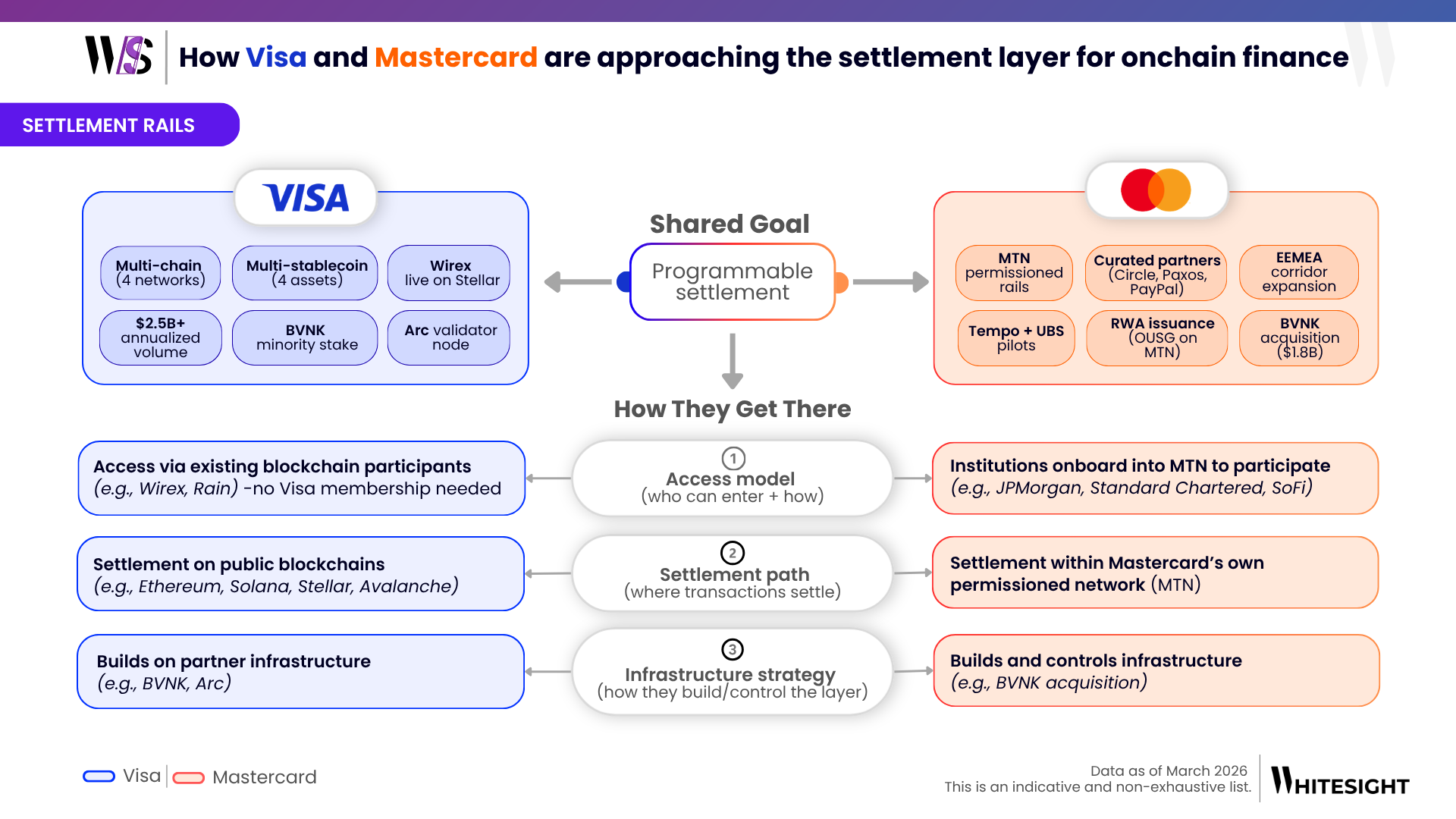

Visa and Mastercard are moving toward the same destination in onchain finance, programmable settlement. But their routes reveal two very different strategic philosophies. Visa is taking an open-rails, partner-led approach that extends its network into public blockchains, while Mastercard is leaning into a more controlled, permissioned settlement layer through MTN, curated partners, and owned infrastructure.

Visa and Mastercard’s onchain strategies show that the next phase of payments competition is shifting below the customer-facing layer and into settlement infrastructure. Visa is positioning itself as an open connector across public blockchains, stablecoins, and crypto-native partners, giving it breadth and flexibility across emerging rails. Mastercard, meanwhile, is building a more controlled institutional environment through MTN, curated participation, and infrastructure ownership.

Actionable insights on fintech, delivered regularly. Join Radar for exclusive fintech content and member benefits.

Don’t miss out on the next big fintech wave! Follow us on LinkedIn and subscribe to our Future of Fintech Newsletter to be the first to know about the Next Big Fintech Strategies.

Don’t miss out on the next big fintech wave! Follow us on LinkedIn for daily updates and in-depth analysis. Subscribe to our weekly newsletter for curated insights delivered straight to your inbox. Unlock exclusive access to our membership plans for deeper dives into market trends, competitor analysis, and investment opportunities.

Login to access Fintech intelligence

Sign up to access Fintech intelligence