Across Latin America, credit has long been a privilege unevenly distributed. In a region where large swathes of the population remain outside formal financial systems, access to credit is often gated by high interest rates, fragmented infrastructure, and a dependency on legacy banking models that haven’t kept pace with consumer needs. Even in high-growth fintech markets like Brazil or Colombia, meaningful inclusion remains patchy, marked by a growing appetite for digital services but constrained by uneven reach.

In the same way, Mexico isn’t new to credit. It just never had enough of it in the right places.

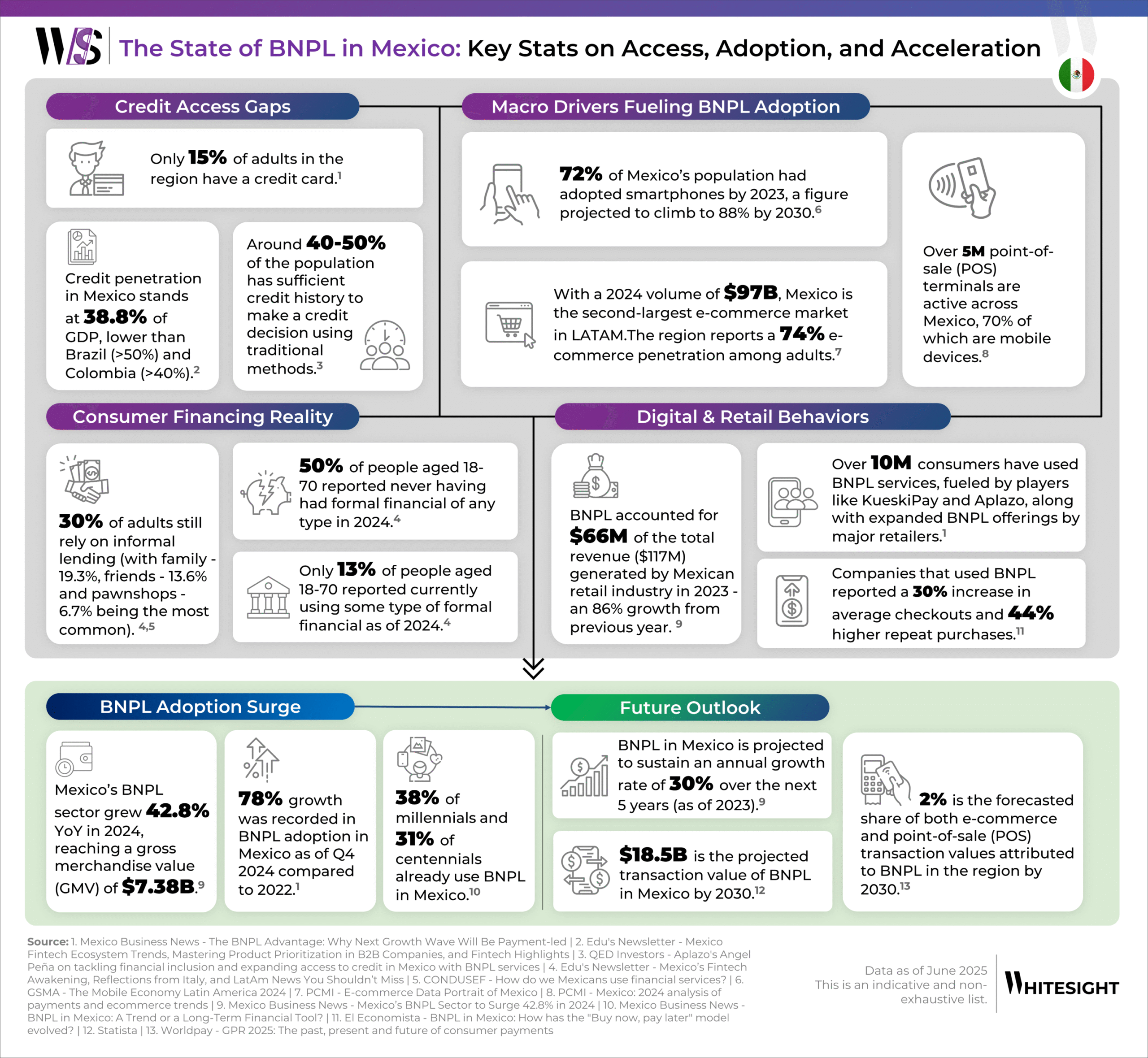

Despite being LATAM’s second-largest economy, most consumers still operate outside the boundaries of formal finance. As of 2024, only 15% of adults own a credit card, and nearly 50% of the population aged 18 to 70 has never accessed any formal financial service. A staggering 30% continue to rely on informal credit, often borrowing from family and friends or pawnshops to cover short-term needs.

It’s in this credit vacuum that buy now, pay later (BNPL) has carved a place for itself. What began as a checkout convenience is fast becoming one of the most accessible forms of credit in the country. In 2024 alone, BNPL usage grew by 78%, crossing 10 million users, and is projected to sustain 30% annual growth over the next five years.

BNPL’s growth in Mexico is a response to something much more foundational.

The most obvious driver is unmet demand. Traditional credit models rely on formal employment histories and high credit scores – criteria that exclude much of Mexico’s workforce. BNPL flips this equation by offering no-interest, installment-based lending with minimal friction, often requiring nothing more than a smartphone and a valid ID.

Second, the timing couldn’t be more ideal. Smartphone penetration hit 72% in 2023 and continues to climb. At the same time, digital transactions grew 30.5% year-over-year, and e-commerce is surging, with 74% of adults now shopping online. BNPL rides these rails seamlessly, especially among millennials (38%) and centennials (31%), who are already using BNPL services.

Lastly, the infrastructure is catching up. Real-time payments (like Cobro Digital or CoDi), partnerships with merchants, and embedded finance integrations are allowing BNPL to scale in ways traditional lenders can’t. And for retailers, the value is undeniable – higher average checkouts, repeat purchases, and lower cart abandonment rates. As per AMVO, retailers in the electronics and fashion sectors already reported up to 50% of online purchases through BNPL channels in 2024 during promotional periods like Hot Sale or El Buen Fin.

In this blog, we’re diving into what makes Mexico a compelling BNPL market today. Let’s explore who’s leading the charge, how business models are evolving, and why BNPL could become the financial backbone for Mexico’s underbanked future.