Most people experience fintech through polished apps, sleek cards, and instant payments. But beneath every smooth interaction sits an invisible machinery of rails: ledgers, payments networks, KYC engines, card processors, and fraud systems that coordinate billions of dollars across millions of users. It’s this hidden infrastructure layer that’s becoming an arena for competition in modern finance.

Globally, this shift is turning into a massive economic story. The Banking-as-a-Service (BaaS) market, where platforms embed financial products through third-party infrastructure, is projected to grow from $15.9B in 2023 to $64.7B by 2032. This rapid expansion mirrors a broader re-architecture of financial services globally, where BaaS has shifted from a niche enabler to a structural layer in digital finance. We’ve unpacked this transformation in-depth in our Brankas × WhiteSight Banking-as-a-Service report.

In the US, more than 150 banks have plugged themselves into this opportunity over the past few years, offering BaaS partnerships to fintechs and large brands. But fast growth has now collided with intense regulatory scrutiny. Throughout 2024, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corp. and the Federal Reserve issued multiple consent orders against BaaS sponsor banks, flagging issues such as weak third-party oversight, anti-money laundering gaps, and insufficient risk controls. New supervisory expectations have made one thing clear: outsourced infrastructure must now be as safe and compliant as a bank’s own internal stack. The industry has been in the middle of a major reckoning, where BaaS models are being re-evaluated under sharper regulatory lenses. We break down this ‘great unbundling under scrutiny’ in our analysis of the BaaS Backlash and what it means for banks and fintechs.

And that pressure has exposed a structural tension: most fintechs rent their critical infrastructure from third parties, but are increasingly held accountable for risks they don’t fully control. This tension defined much of the embedded-finance narrative in early 2025, as digital brands accelerated into infrastructure partnerships even while regulators tightened the screws. We explore these shifts across banks, fintechs, and platforms in our Embedded Finance (Q1 2025) Roundup.

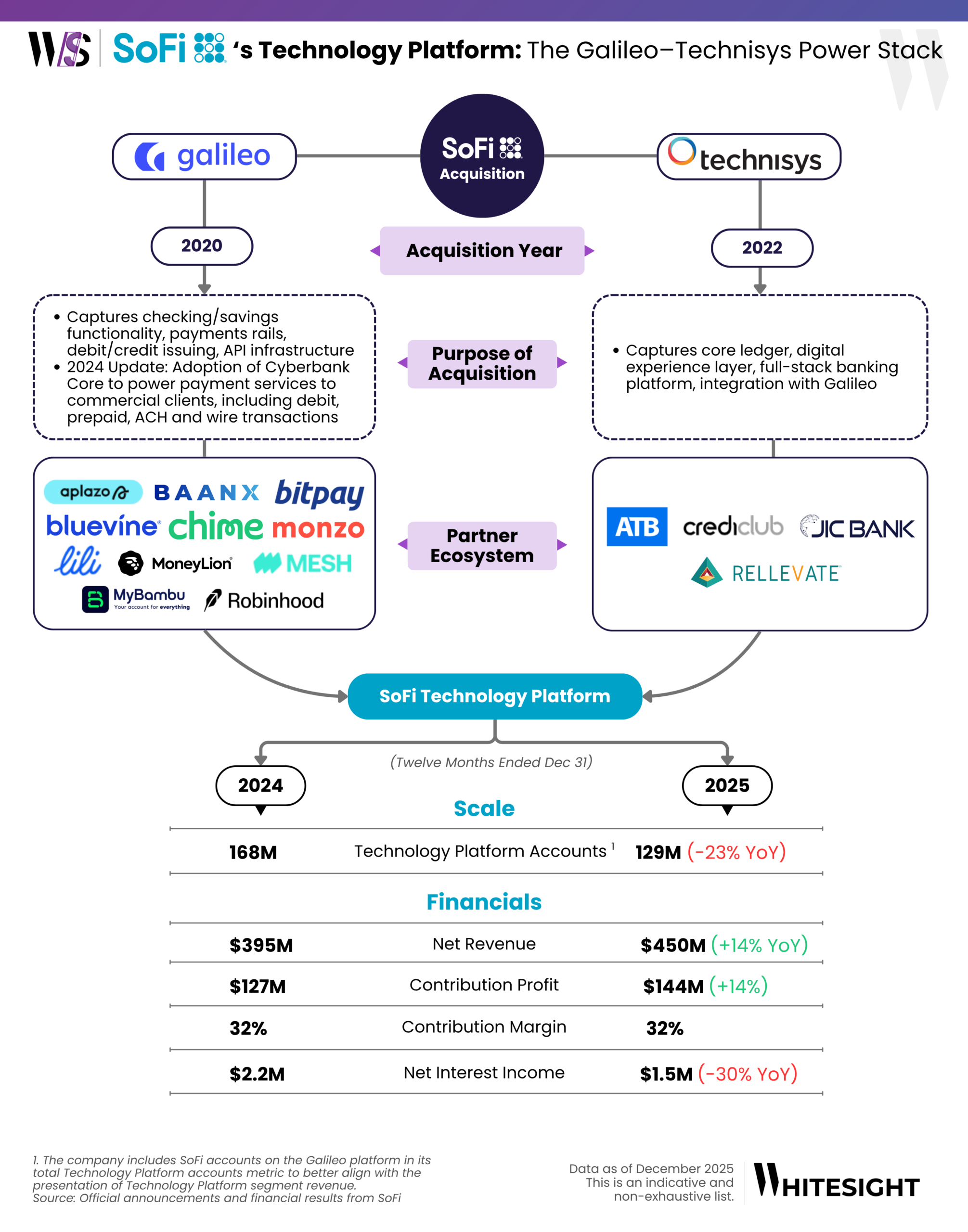

This is where SoFi made a very different bet. Instead of renting the technology that powers its financial products, SoFi bought the infrastructure themselves. It acquired Galileo Financial Technologies, a full suite of open APIs enabling companies to build modern consumer and B2B fintech services – from account setup and payments to card issuing and real-time transaction controls. Then came Technisys, a cloud-native, multi-product core banking platform. Through its Cyberbank system, it provides institutions the ability to design, configure, and manage innovative financial products across deposits, lending, and digital banking. Together, they gave SoFi ownership of the payments layer, the core ledger, and the digital experience engine underneath its products. Today, this same stack not only powers SoFi’s own bank but also serves dozens of fintechs, enterprises, and global financial institutions.

To understand how SoFi is positioning itself as a long-term infrastructure provider, and how its technology platform keeps delivering growth, we need to unpack how Galileo and Technisys work together.

But to become a top-10 financial institution, a goal CEO Anthony Noto articulated, SoFi couldn’t solely rely on just consumer products. Noto emphasized the following pillars: capital strength, regulatory alignment, consumer trust, and most importantly, control over its own infrastructure. That realization became the catalyst for a major strategic pivot.

In 2020, SoFi acquired Galileo for $1.2B. Galileo was already powering SoFi Money through its programmable APIs for account setup, card issuing, payments, fraud controls, and sandbox testing. Instead of renting this backbone, SoFi brought it in-house, instantly adding a B2B revenue arm and gaining full control over the payments and issuing layer. As Anthony Noto noted at the time, it was SoFi’s own members who pushed the company toward “bigger, bolder, and more expansive thinking”, a mindset that made acquiring Galileo inevitable.

Two years later, it acquired Technisys for $1.1B, adding a cloud-native, multi-product core banking platform designed for modern digital finance. Technisys complemented Galileo by powering the ledger, deposits, lending, cards, and the full digital experience layer – an essential piece of SoFi’s ambition to build the “AWS of fintech.” As Anthony Noto put it, Technisys brought the “Gen-3 core technology every financial institution will need to keep pace with innovation, enabling SoFi to serve millions more customers and partners worldwide”.

Together, Galileo and Technisys form SoFi’s end-to-end, vertically integrated Technology Platform stack. Galileo let SoFi support product expansion for partners across the US, Canada, Mexico, and Colombia, while Technisys further expanded its operations into LATAM. This combined footprint has turned SoFi into a true B2B infrastructure player, tapping a $4.1T embedded-finance market and powering brands like Chime, MoneyLion, Robinhood, Crediclub, and Rellevate.

Since then, both platforms have expanded rapidly across products, geographies, and marquee partnerships:

All of this expansion shows up clearly in the Technology Platform’s financials. From 2023 to 2024, segment net revenue rose from $352M to $395M, while contribution profit climbed from $95M to $127M. These gains come from a simple dynamic: the platform earns fee-based revenue every time an account is opened or a payment moves, and because the infrastructure is already built, each new transaction adds revenue with minimal cost.

Growth has been driven from three places: stronger adoption by existing partners, new high-volume programs (like Direct Express), and SoFi’s own migration onto Cyberbank Core.

Even the modest 1% dip in enabled accounts in 2025 didn’t slow the segment’s trajectory. Revenue still grew double digits year-over-year, and contribution profit remained healthy. This is thanks to the high-volume partnerships (like Southwest Airlines, Wyndham Hotels, and the U.S. Treasury) that generate significantly more activity per user than many early fintech clients. Meanwhile, LATAM banks such as Banco Nación bring large, stable customer bases that deepen the platform’s international footprint.

As SoFi shifts more of its own banking stack onto Galileo and Technisys, the platform benefits twice by earning external revenue from partners while reducing SoFi’s internal reliance on third-party vendors. That dual effect explains why the Technology Platform segment continues to deliver consistent revenue growth, rising profitability, and expanding margins from 2023 through 2025, even in a competitive and increasingly regulated infrastructure landscape.

Join Radar for exclusive member benefits and access to expert reports, industry trend breakdowns, and insights on everything from Embedded Finance to Digital Banking, Open Finance and beyond.

SoFi’s Technology Platform is steadily becoming the engine that positions it as a long-run leader in embedded finance. By giving financial and non-financial brands plug-and-play access to payments, lending, and digital banking rails, SoFi is turning into the infrastructure layer other institutions build on. As embedded finance is expected to witness a CAGR of 16.8% through 2029, Galileo’s expanding roster of high-profile clients create stronger network effects, more predictable revenue, and deeper enterprise reach. With two of its largest brand partnerships set to launch in 2026, as revealed by Noto in the Q3 2025 earnings call, Galileo is shaping SoFi’s evolution into a foundational layer of the future financial system.

Unlock the deep dives into the winning strategies of Nubank, Monzo, Revolut, and more with a WhiteSight Radar Membership.

Don’t miss out on the next big fintech wave! Follow us on LinkedIn and subscribe to our Future of Fintech Newsletter to be the first to know about the Next Big Fintech Strategies.

Authors

Already a subscriber? Log in to Access

Radar Subscription

Select a membership plan that resonates with your

goals and aspirations.

Not Ready to Subscribe?

Experience a taste of our expert research with a complimentary guest account.

AI Agents Are Killing Checkout. Stripe and Adyen Are Racing to Own the Aftermath ‘Reorder my usual coffee.’ Your agent...

A couple of weeks ago the headlines crowned Nik Storonsky Britain’s almost-richest man. A Musk-style pay deal that could be...

Login to access Fintech intelligence

Sign up to access Fintech intelligence