Small and medium-enterprise (SME) banking is the original fintech origin story: one of the most important customers, treated like the world’s most inconvenient ones. Their business runs in real time: orders, payroll, inventory, refunds. Yet, the traditional bank experience still too often starts with a polite request for last year’s PDFs and a side of collateral.

That mismatch matters because SMEs are not a niche. Globally, SMEs make up 90%+ of all businesses, drive ~70% of employment, and contribute ~50% of GDP.

Incumbents have long known that SMEs matter. The challenge has been translating that awareness into service at scale. Why? Because most incumbents are optimised for two extremes: standardised retail at scale, and well-documented corporates with formal histories. SMEs live in the messy middle – often “data-thin” on paper, yet rich in real-time insights across POS, eCommerce, invoicing, and payment flows.

And even banks admit the infrastructure is a constraint. A 2024 IBM survey flags lack of modularity in core banking systems (53%) and inadequate API standards (52%) as major barriers to evolving SME offerings.

Meanwhile, SMEs moved on. The pandemic accelerated a behavioural reset: IDC notes over 90% of SMBs increased their reliance on technology, making digital adoption “a matter of survival”. As they go digital, expectations are rising. They now demand seamless, omnichannel experiences from financial providers. “Banking basics” like fast onboarding, low-friction transactions, and real-time decisions stop being differentiators and become table stakes.

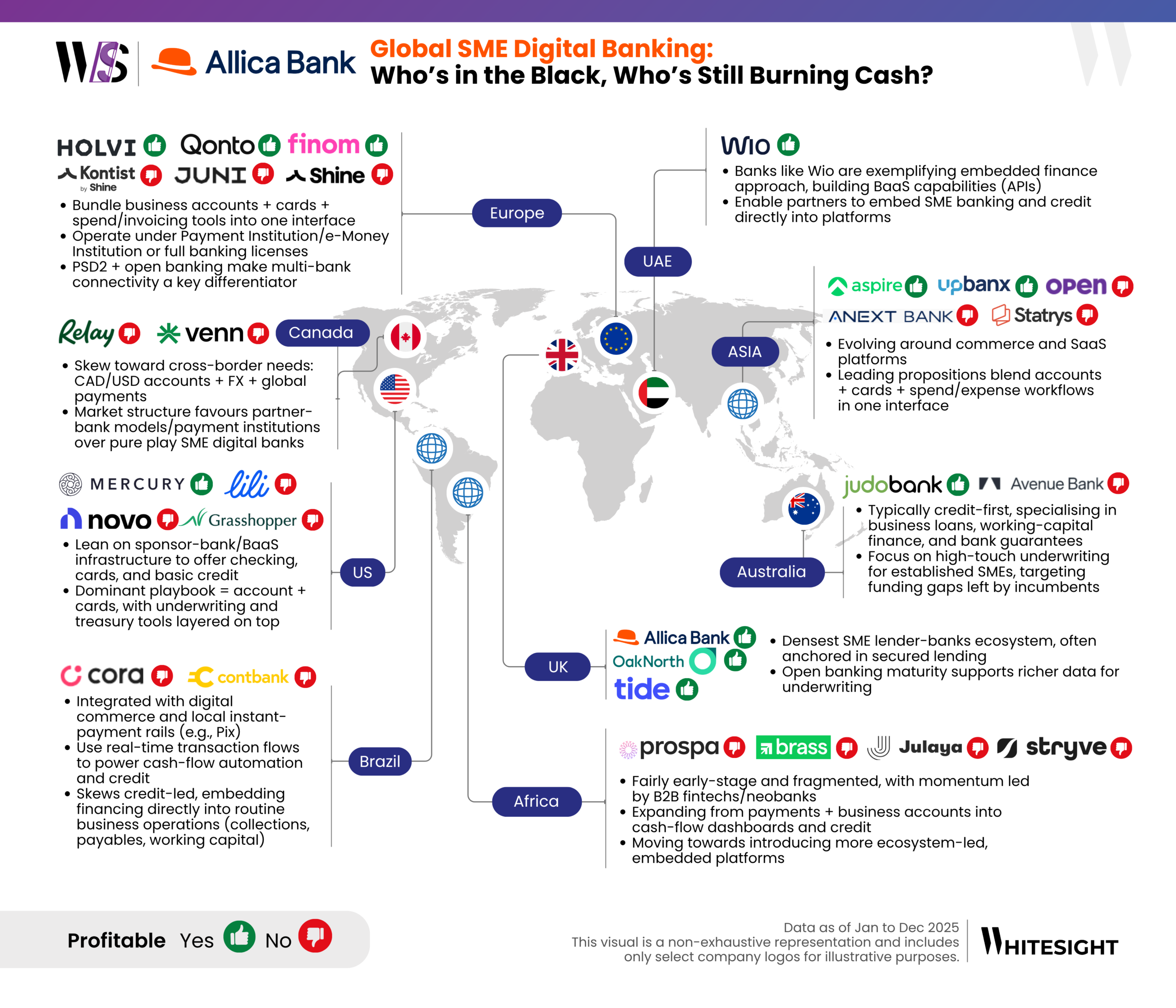

This is exactly where a new generation of SME banking models has emerged, because the gap is now too visible, too expensive, and too ripe for unbundling. SME digital banking is diverging across markets – API-powered SME stacks in mature economies, and workflow-native models in emerging markets are creating entirely new playbooks. Our report Reimagining Digital Banks for SMEs with Zazu explores this distinction in further detail.

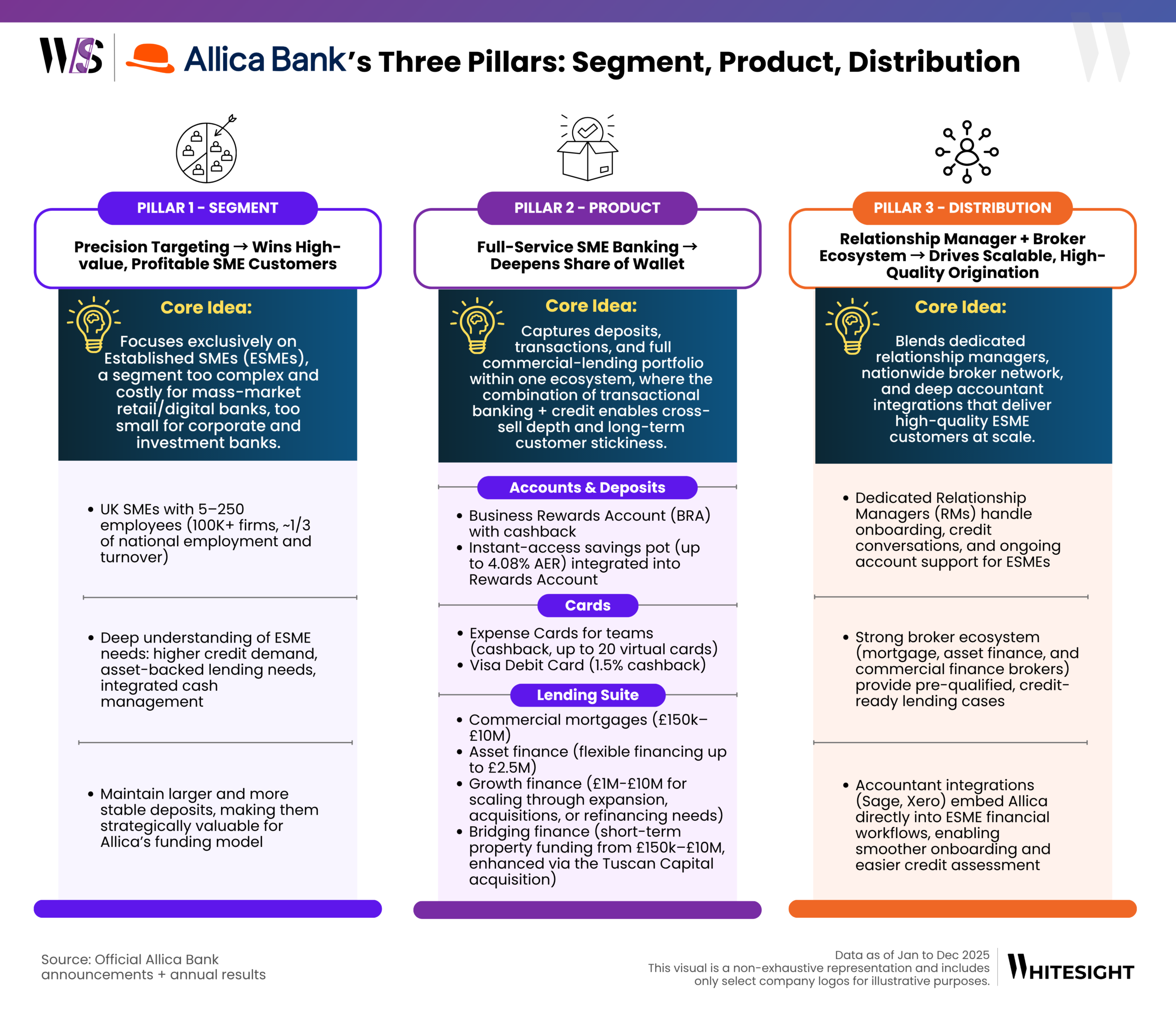

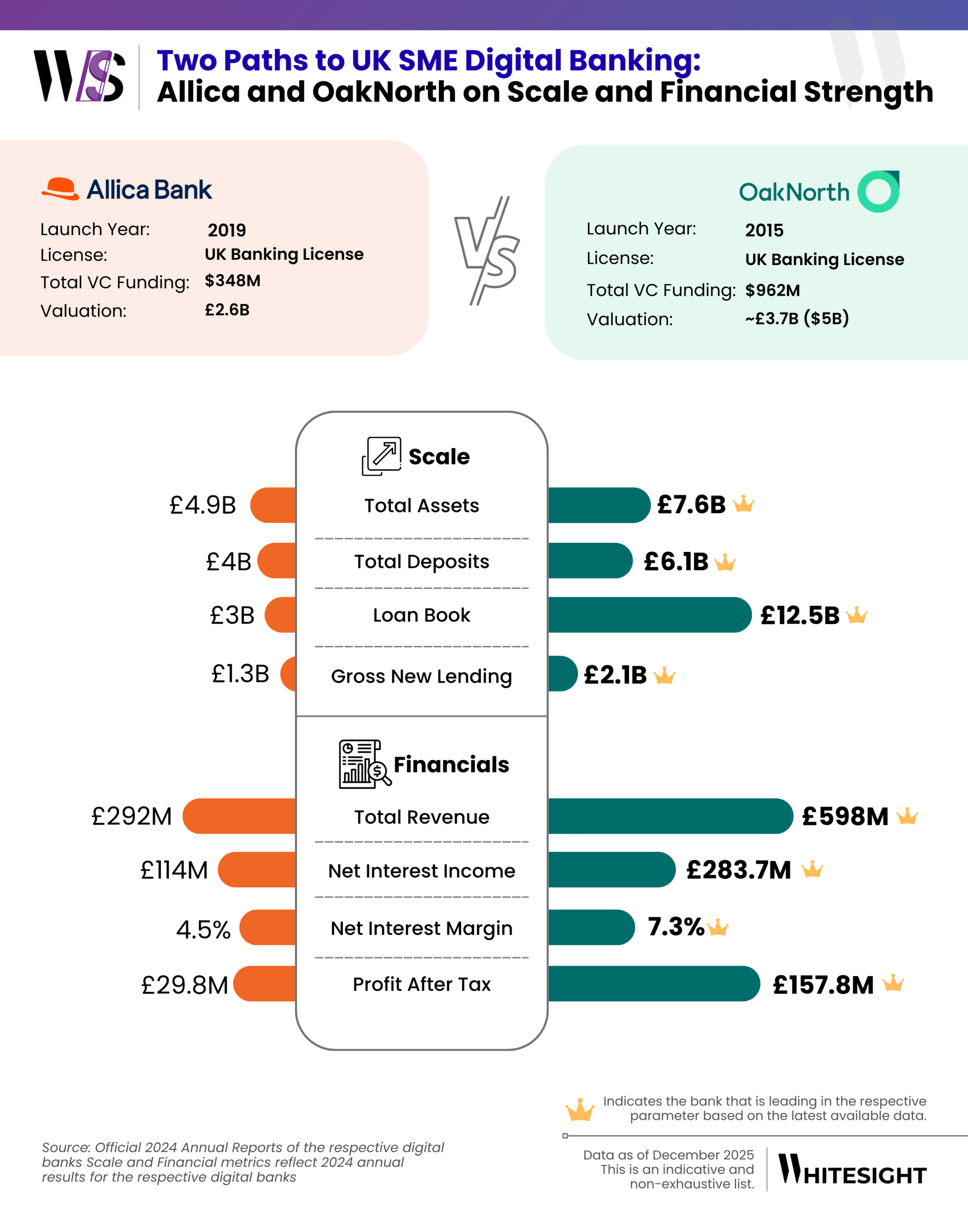

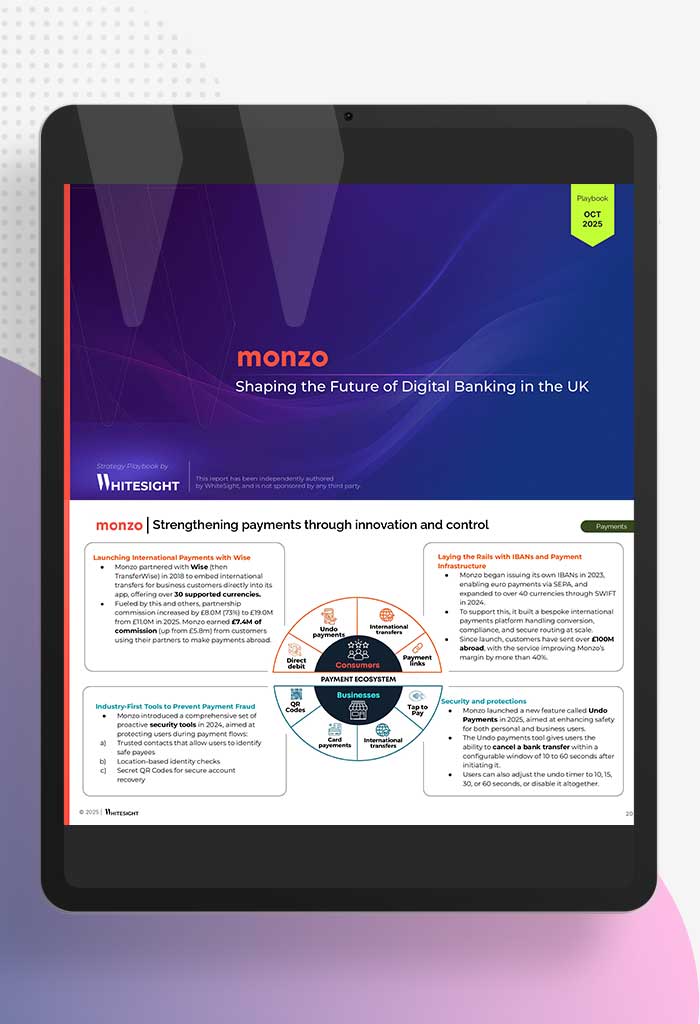

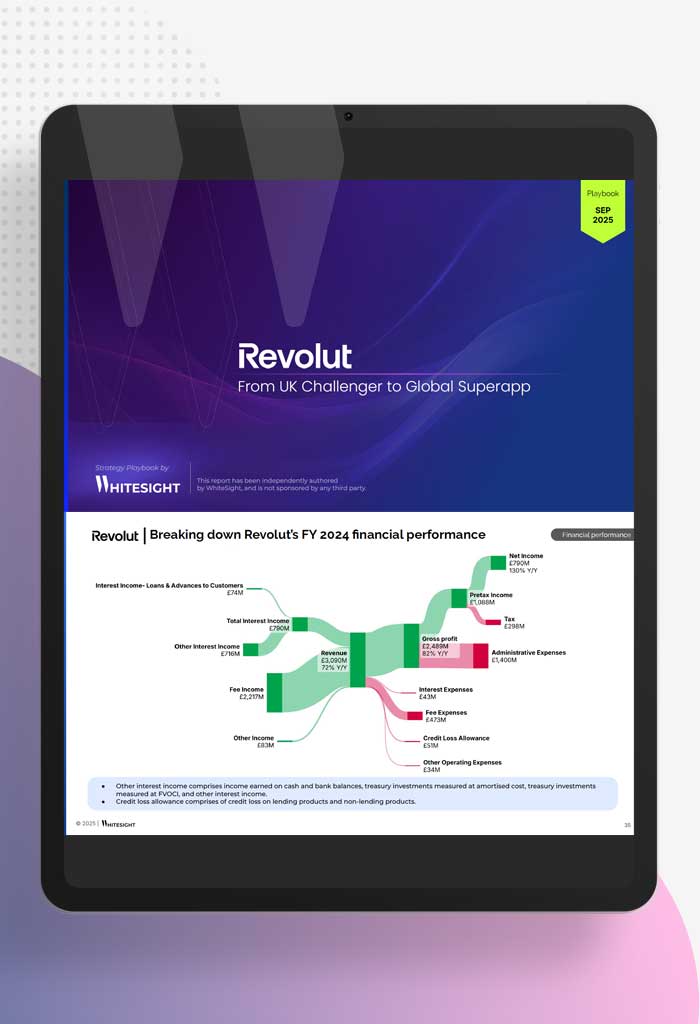

On one side, players from adjacent strongholds have expanded to cater to SMEs. This includes retail digital banks that are layering business banking tools onto existing infrastructure like Revolut, which has launched a business account that allows SMEs to manage their finances, send and receive payments, and access a range of other financial tools. Its SME push is a moat strategy, using merchants and business tools to build recurring revenues, something we explore in-depth in our Revolut: From UK Challenger to Global Superapp deep dive. Similarly, Nubank has launched a range of credit products, such as overdrafts and loans, that are tailored to the needs of SMEs. Its SME expansion shows how retail-first players port their distribution advantage into business banking by bundling banking, lending, payments, and financial management tools. Our work on Nubank’s SME Expansion (4 Key Offerings) decodes this further. Others like Allica Bank, OakNorth, and Qonto were built SME-first. These digital banks design workflows with multi-user accounts, real-time cashflow visibility, integrated payments, and credit built on operating data, whether via a licence or sponsor-bank/BaaS rails.

And adoption is already visible in financial services. A 2025 OECD D4SME survey reveals that 58% of SMEs use digital financial services from fully digital fintech providers, led by online banking (43%) and payment processing (42%).

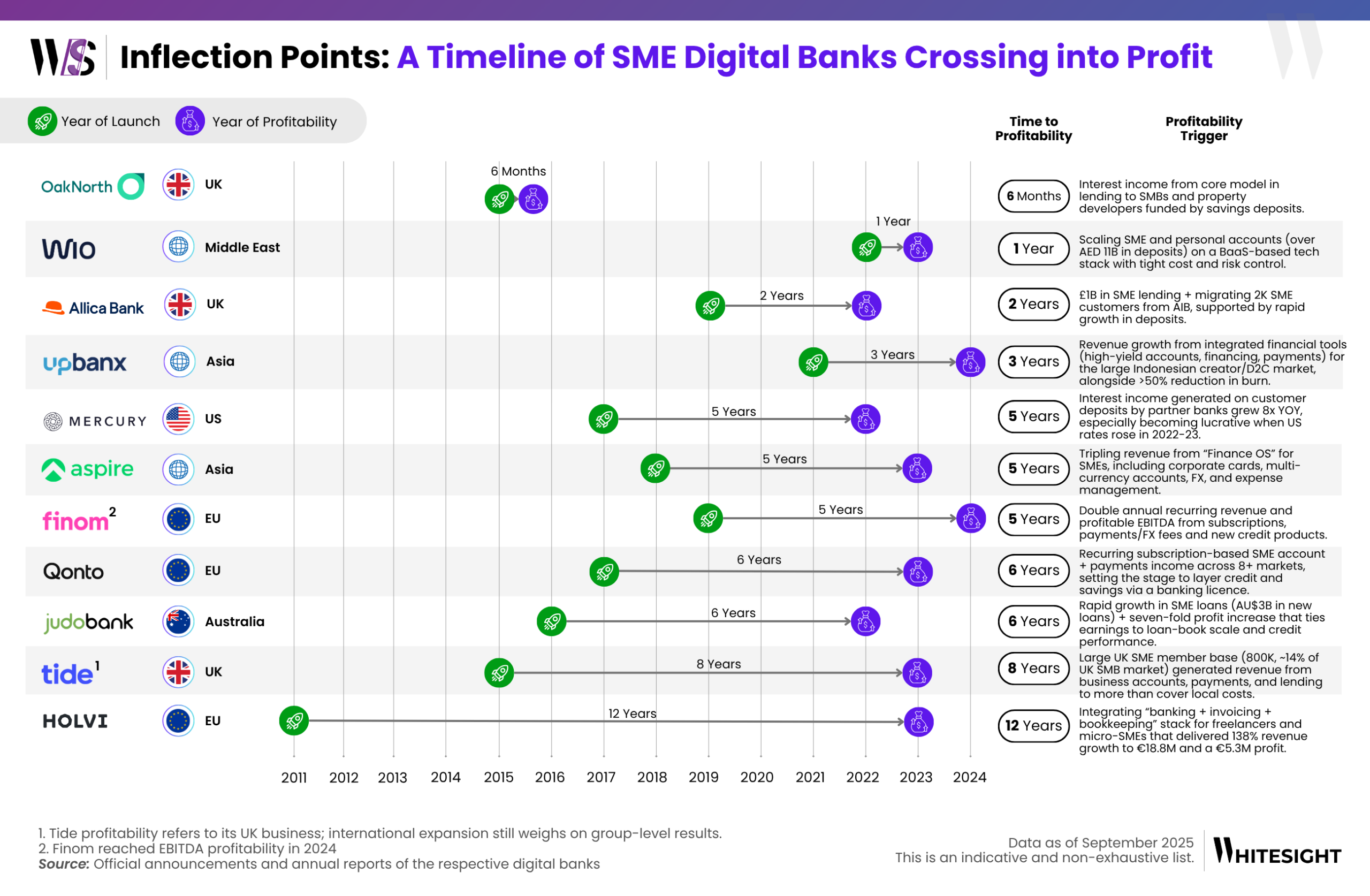

But with this comes the question of the hour: it’s one thing to serve SMEs, can challengers do it profitably, at scale, and through cycles?