When digital banks first emerged around 2010–2015, their goal was simple: make banking fast, fair, and frustration-free. Slick onboarding, transparent fees, and human-centred design turned finance from a chore into a choice. Yet as user bases scaled, expectations evolved. Today’s digital banks no longer stop at current accounts, savings, or loans. They’re building multi-product platforms that extend into insurance, investments, e-commerce, and even lifestyle utilities like travel perks and e-SIM connectivity.

The logic is clear. 57% of consumers prefer super apps for the convenience of unified services on one platform. Digital banks sit at the centre of that appeal, with users showing the strongest interest in integrating mobile purchases (54%), money transfers (53%), and bill payments (51%) within the same app. What’s more, PYMNTS Intelligence finds that 79% of banks are preparing for a “deeply embedded” future, with 70% viewing this integration as core to their digital strategy.

The transformation is taking visible shape across markets. In Asia, super apps like WeChat, Alipay, and Gojek have created ecosystems where payments, shopping, and social experiences coexist seamlessly. In Brazil, Banco C6 exemplifies this shift with a full-stack superapp that unifies banking, credit, insurance, and investments. It has targeted the upmarket segment by offering curated investment products in partnership with JPMorgan Chase for high-net-worth clients, a strategy we’ve uncovered in our Banco C6 Strategy Playbook. Meanwhile, Nubank’s no-fee credit card, paired with features like PIX transfers, remittances, and embedded telecom services, shows how digital banks can unlock inclusion and profitability at scale, as explored in our Nubank Deep Dive report.

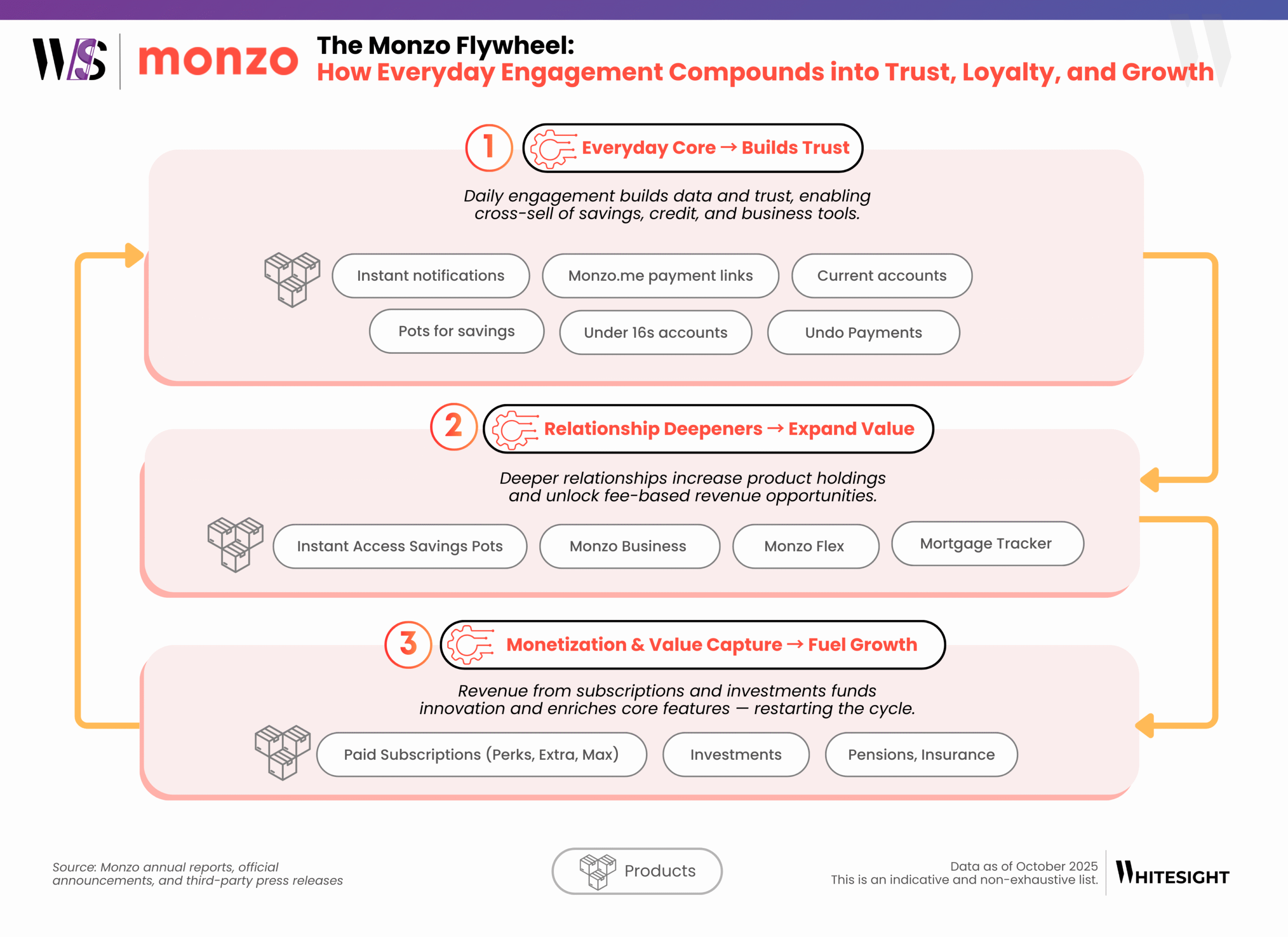

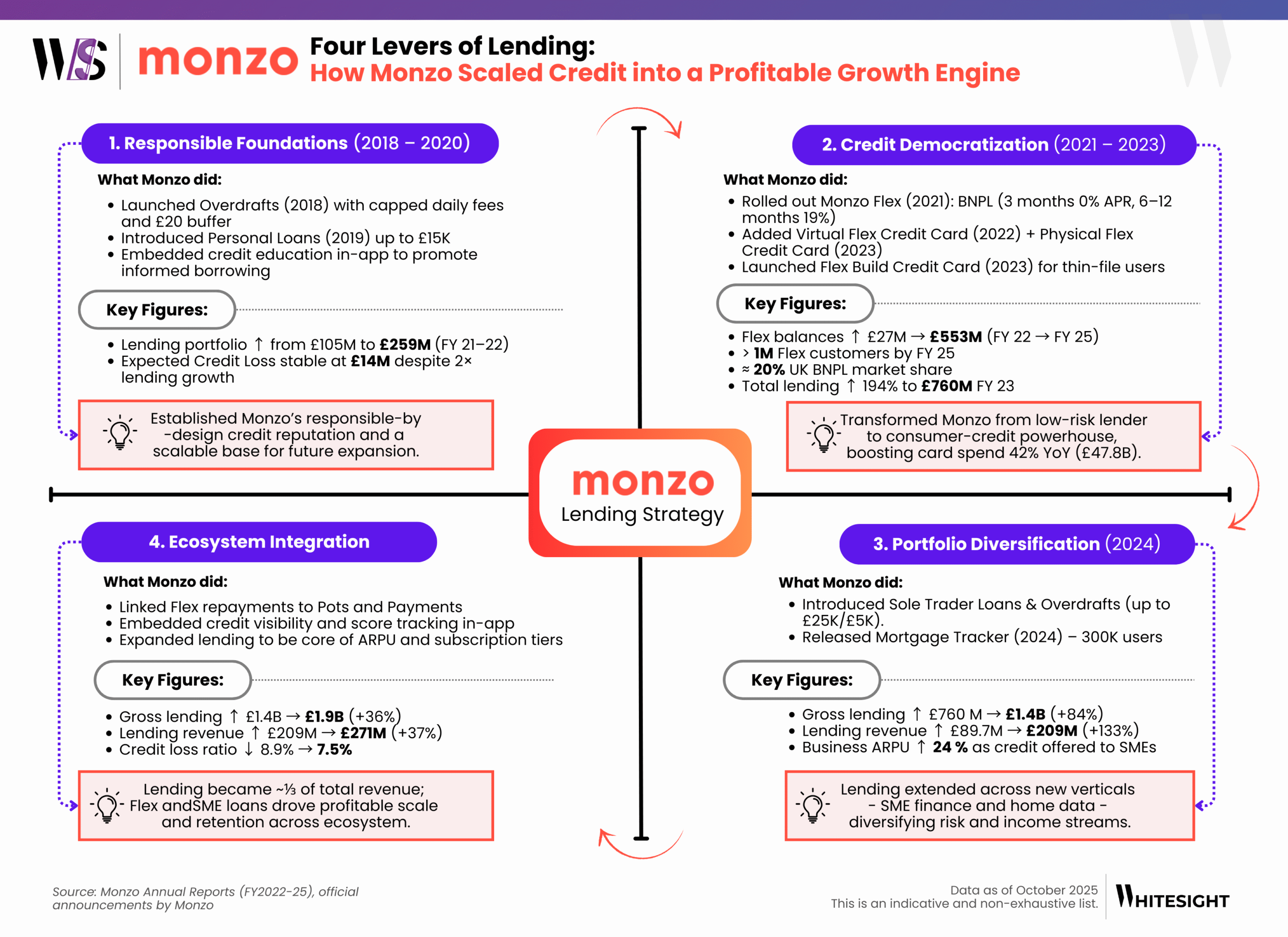

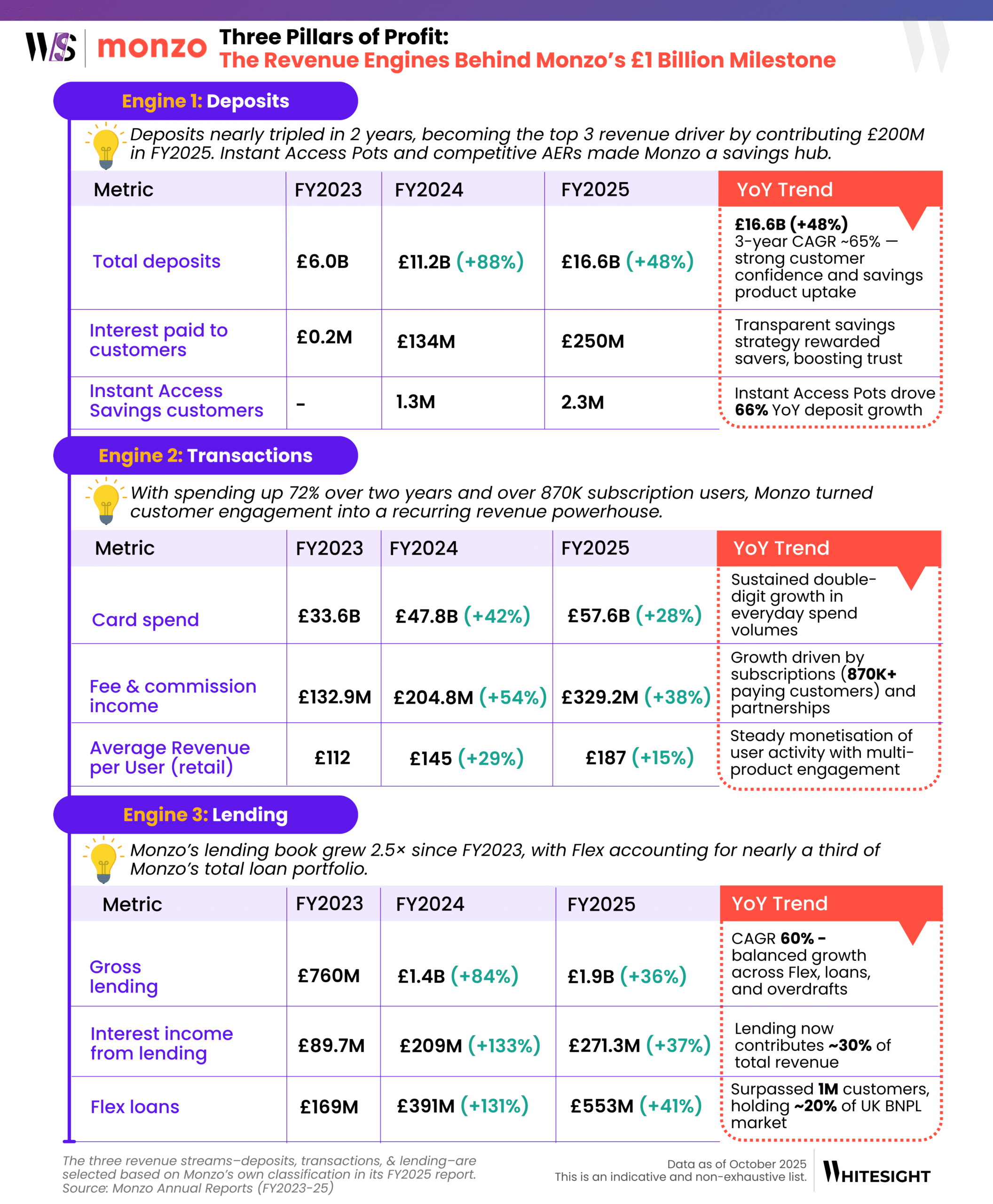

The UK is seeing the same wave. In fact, 57% of UK consumers say they would trust their bank to deliver such an integrated financial super app. Revolut, with 65M+ customers worldwide, has taken this ecosystem vision global. It has turned its borderless finance model into a global super app, from cross-border transfers to travel, crypto, and lifestyle subscriptions. Our Revolut: From UK Challenger to Global Superapp playbook covers its transformative path in detail. Monzo, meanwhile, is pursuing depth over breadth, positioning itself as a “financial control center” where consumers can manage their financial lives.

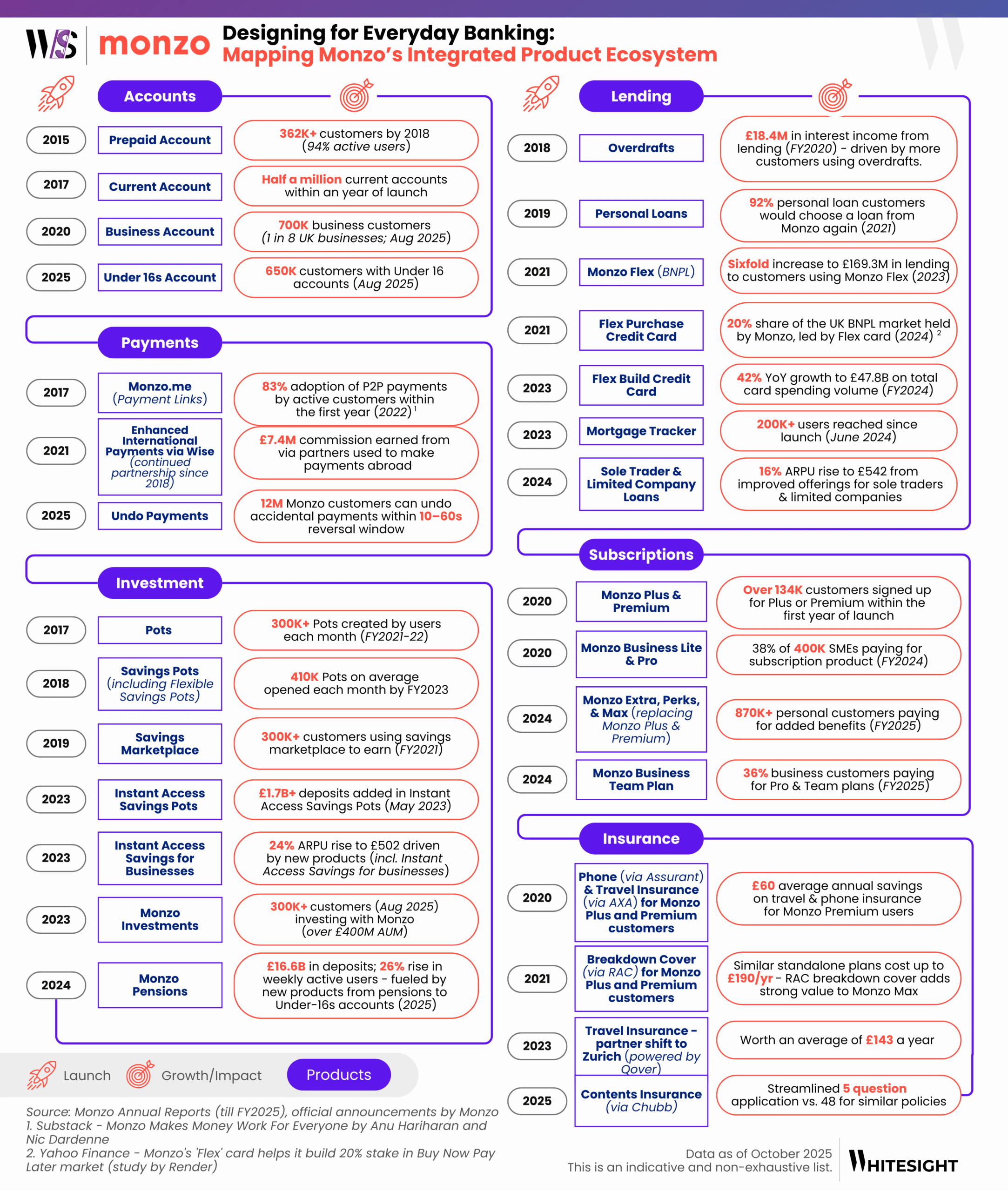

What’s emerging is a deliberate layering of value, built for retention, monetisation, and scale. And it’s this philosophy that frames Monzo’s evolution across three arcs: product evolution, business growth, and financial growth.