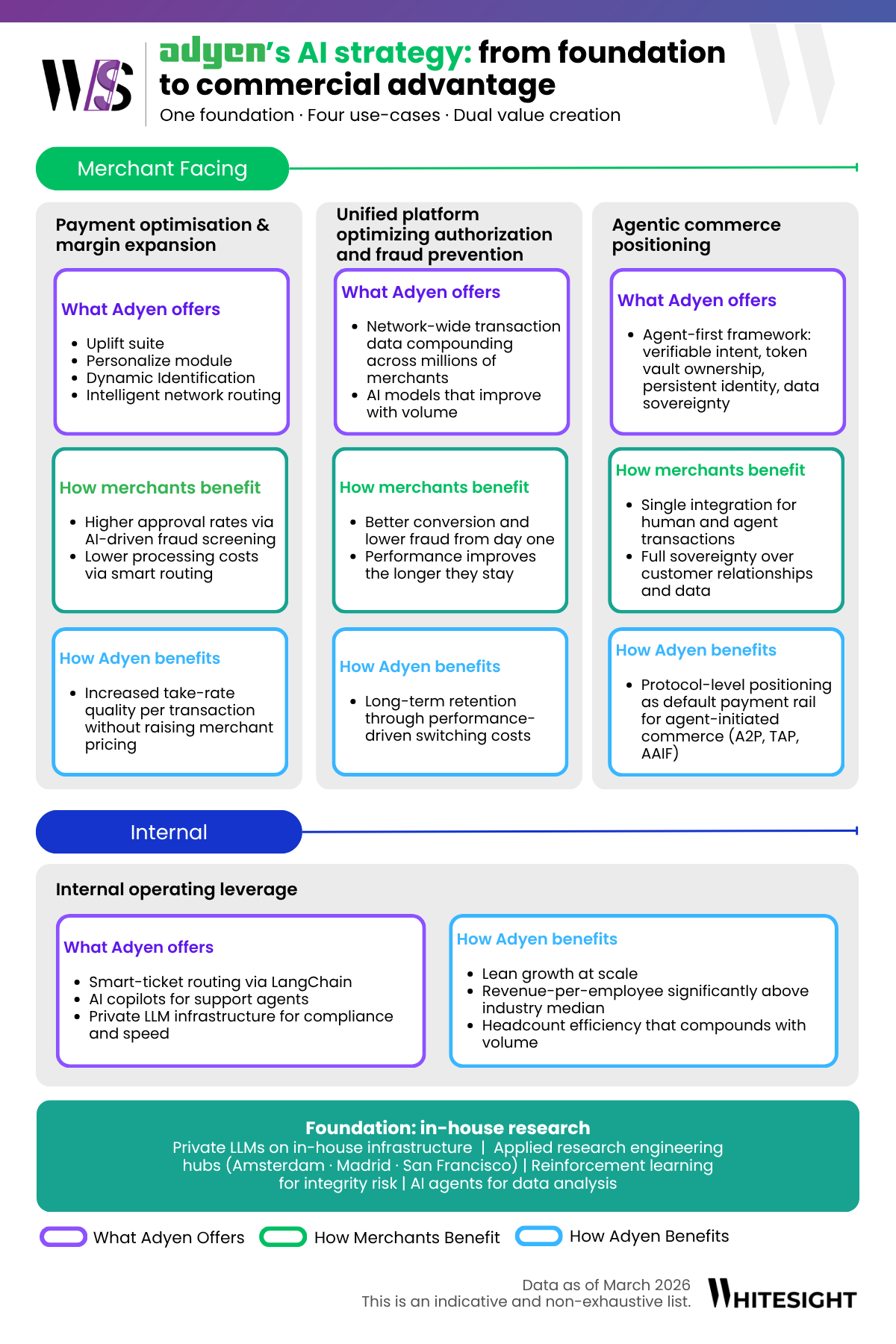

For decades, merchants had to choose between three conflicting goals: maximising conversion, minimising fraud, and lowering costs. Boosting one usually damaged the others. Tighter fraud rules blocked legitimate customers. Cheaper processing routes had lower approval rates. Merchants were stuck making trade-offs with no way to optimise the full payment funnel at once.

- Recognising the shopper before they click pay:

In February 2026, Adyen expanded Uplift with Personalize, a module that adapts the checkout page in real time for each shopper. Traditional checkouts are static; every customer sees the same payment methods in the same order, regardless of their history or preferences. Adyen’s research found that 37% of shoppers abandon a purchase if the process takes too long.

Personalize works through what Adyen calls Dynamic Identification. When a shopper reaches checkout, the system cross-references their signals, device, location, browser, and card token against Adyen’s network-wide transaction data. Within milliseconds, it determines who the shopper is, what payment method they’re most likely to use, and how much security friction they actually need. A returning customer with a clean history might see Apple Pay at the top and skip 3D Secure entirely. A first-time visitor from a high-risk location might see additional verification. The checkout configures itself before the customer begins typing.

This also works in the merchant’s favour in terms of cost. Not all payment methods carry the same processing fees. When a shopper is equally likely to use a debit card or a credit card, Personalize presents the cheaper option more prominently. This reduces the merchant’s transaction cost without adding friction for the customer. As Carlo Bruno, Adyen’s VP of Product, puts it: “Personalize achieves this balance by using Dynamic Identification to recognise shoppers instantly. This allows us to tailor the journey from the very first step.”

- Filtering fraud without blocking real customers:

Once a shopper clicks “pay,” the transaction enters fraud screening. Traditional fraud prevention relies on manual rules, written by human analysts and applied uniformly to every transaction. “Decline anything above $500 from a new account.” “Flag all transactions from certain countries.” These rules cast a wide net, but they inevitably catch legitimate customers alongside actual fraudsters.

Uplift replaces this with AI models that evaluate each transaction individually, weighing hundreds of signals in real time to distinguish genuine shoppers from synthetic fraud. Because Adyen has already seen most of the shoppers through other merchants on its platform, the system starts with a baseline of trust. The models learn continuously from every transaction across the network, adapting to new fraud patterns without waiting for a human analyst to write a new rule. Pilot enterprise customers reduced their manual risk rules by 86% on average, with 35% eliminating them. False positives, legitimate transactions incorrectly blocked, dropped by 42%.

- Converting more transactions into successful sales:

Smarter fraud screening feeds directly into higher conversion. When the system correctly identifies a legitimate shopper, it can reduce unnecessary security steps. These include skipping 3D Secure challenges, avoiding redundant verification, and fast-tracking approval. The shopper experiences less friction. The merchant makes more sales. Uplift has helped over 6,500 businesses achieve an average conversion rate 1.19% above industry baselines, with some merchants seeing gains as high as 6%.

- Routing every transaction through the cheapest viable network:

Once a transaction is approved, it needs to travel through a processing network to reach the shopper’s bank. Each network, Visa, Mastercard, STAR, NYCE, PULSE, Accel, charges different fees and has different approval rates. These depend on the card issuer, the transaction type, and the merchant category. Before Uplift, most merchants either defaulted to premium networks or used basic, least-cost routing.

Uplift’s routing AI evaluates each transaction individually, factoring in the card issuer’s historical behaviour on each network, the fee structure, and the transaction characteristics. It then selects the route that minimises cost without sacrificing approvals. In its first year, Uplift helped businesses lower payment costs by 9.4% on eligible traffic.

- Reshaping the economics of debit:

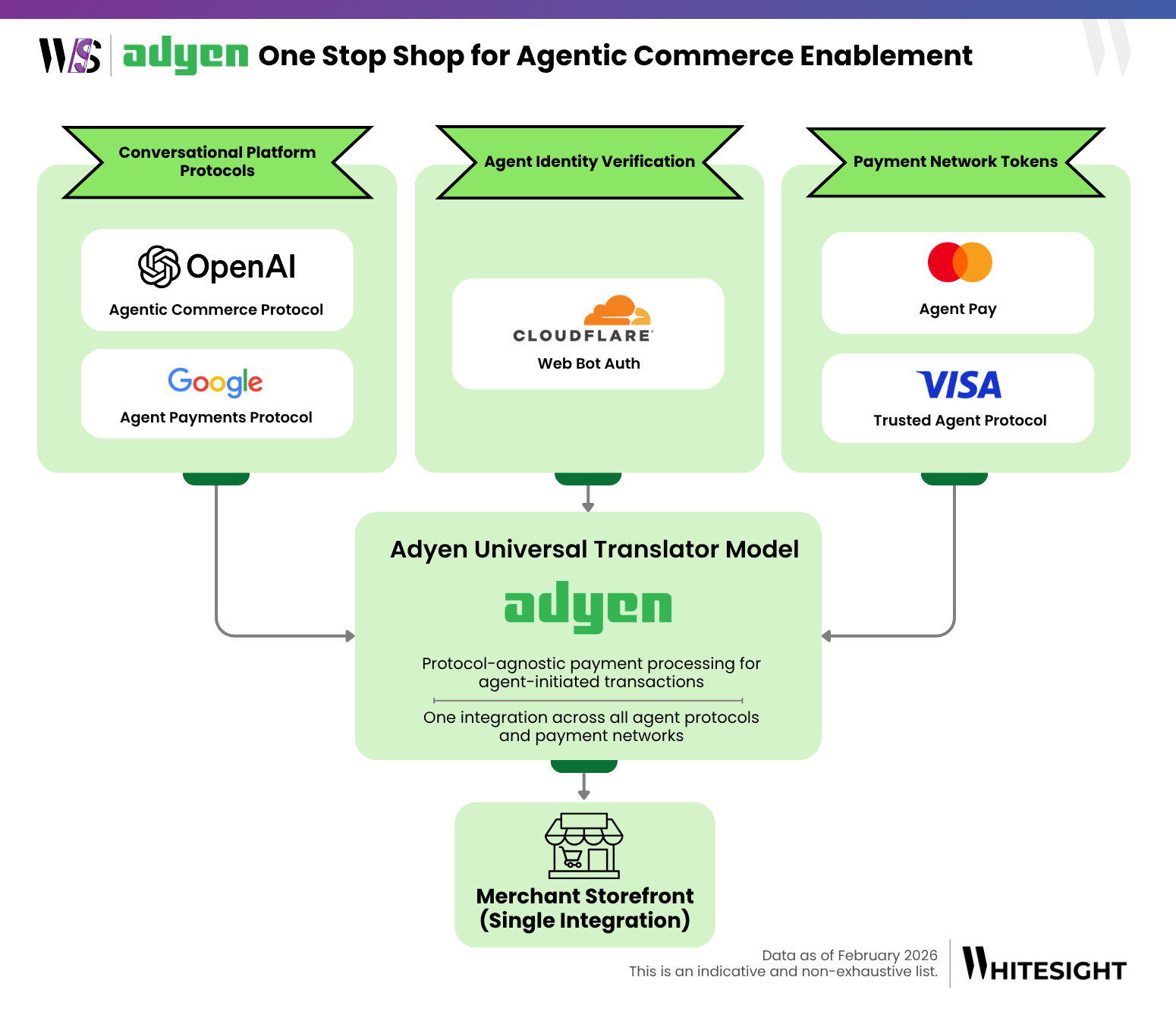

A standout application of this routing intelligence is Intelligent Payment Routing for US debit. Since the Fed’s 2023 clarification, US regulation requires every debit card to work on at least two unaffiliated networks, giving merchants a choice on every transaction. Adyen’s AI makes that choice in real time, analysing which network will approve this specific debit transaction at the lowest cost. In a pilot with over 20 enterprise merchants, including eBay, Microsoft, and 24 Hour Fitness, the system showed strong results. It achieved an average of 26% cost savings, with some high-frequency retailers reaching 55%. One customer saved $600,000 within the first 30 days.