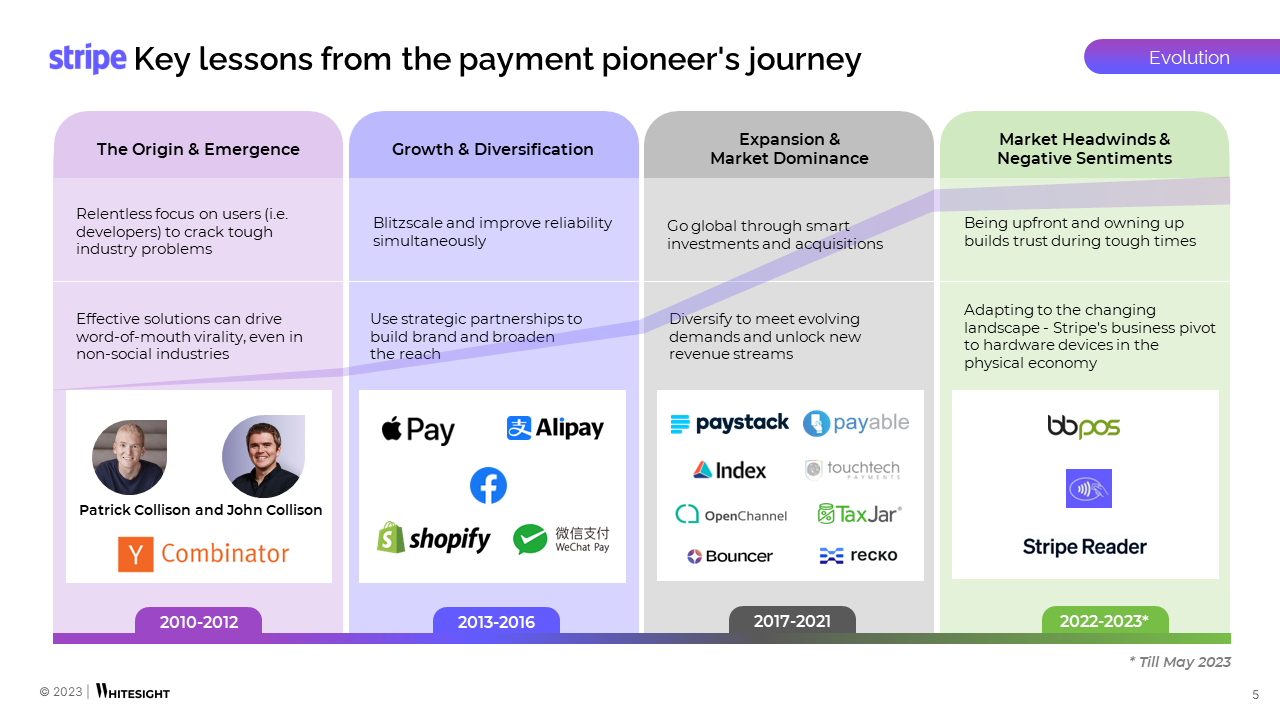

2022 brought a noticeable shift pertaining to market headwinds after the successful fintech boom of 2021, prompting Stripe to adjust its approach and embrace products from diverse sectors, including:

- Crypto Payouts (2022): to allow businesses to send cryptocurrency payouts to sellers, freelancers, creators, and service providers globally.

- Financial Connections (2022): to let businesses establish direct connections with their customers’ bank accounts that power various financial processes, including verifying bank accounts, checking balances, and confirming account ownership.

However, despite its lofty beginnings, the payments giant has since had to reassess the value of its shares, first plummeting to $74B in July 2022, accompanied by a layoff of 14% of its workforce in November 2022, before taking another hit and sinking even lower to $63B in January 2023.

Notably, these recent valuations of Stripe were determined through a 409A internal valuation process, which is regulated by the Internal Revenue Service and conducted by an independent appraiser. This process sets a fair market value without influence from venture capitalists or other investors. Interestingly, Stripe conducts these evaluations more frequently than the usual annual norm.

Nevertheless, Stripe continues to make significant progress and introduce exciting new developments. In March 2023, it rolled out its Tap to Pay feature on Android, giving businesses in six countries the ability to accept contactless in-person payments via a compatible phone or tablet. More recently, Stripe raised $6.5B in a Series I funding round at a $50B valuation to provide liquidity to employees and address tax obligations related to equity awards. They have also ventured into artificial intelligence, partnering with OpenAI to integrate the GPT-4 model into their products and services. In turn, OpenAI will leverage Stripe’s payments platform to power payments for ChatGPT Plus and DALL·E.

The Stripe Strategy: Bold Ambition or a High-Stakes Game?

Stripe’s product strategy is undeniably impressive, driven by a new guiding framework that is both bold and ambitious. However, with the addition of building for numerous engineering teams, there is a risk of overreaching and launching a product that needs more impact.

Although Stripe has an extensive payment network that spans 197 countries, offering ample opportunities to contribute to global commerce, build a loyal customer base, and explore new revenue streams such as BaaS and Financial Connections, there are still many challenges on the horizon for this payments provider.

In the competitive payments industry, pricing pressure and the rise of open banking’s account-to-account payments pose further challenges to traditional card payment models. Several startups, such as Adyen, Razorpay, are also replicating Stripe’s successful approach in their home markets, while tech platforms are building their own payment systems to reduce fees and increase control.

Amidst new ventures, Stripe seems to be seeking lucrative revenue streams. The question looms large: Will they pursue an IPO or delay it? Facing a significant tax bill in 2023 from restricted stock units (RSUs) distribution and rumours of a quest for profitability, Stripe’s balance in the competitive fintech landscape will be captivating to observe.

Quick View

Quick View Quick View

Quick View