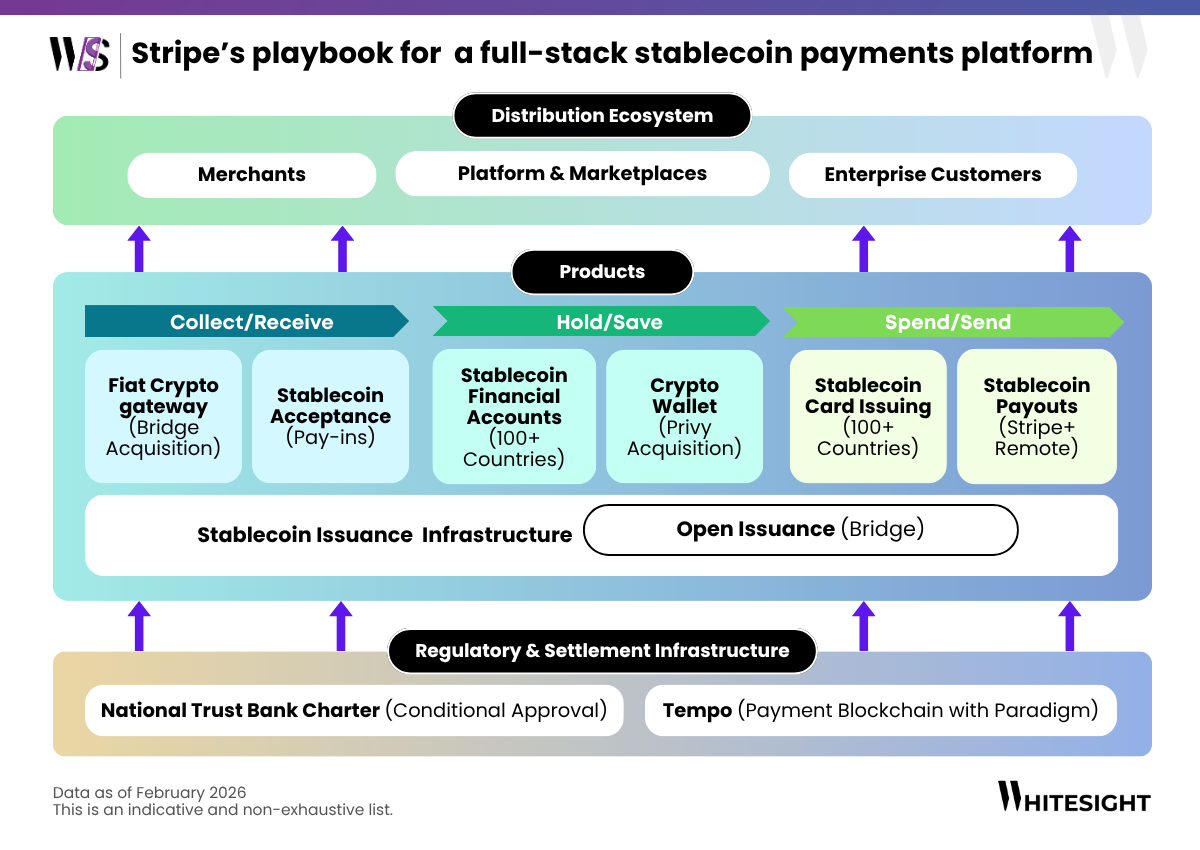

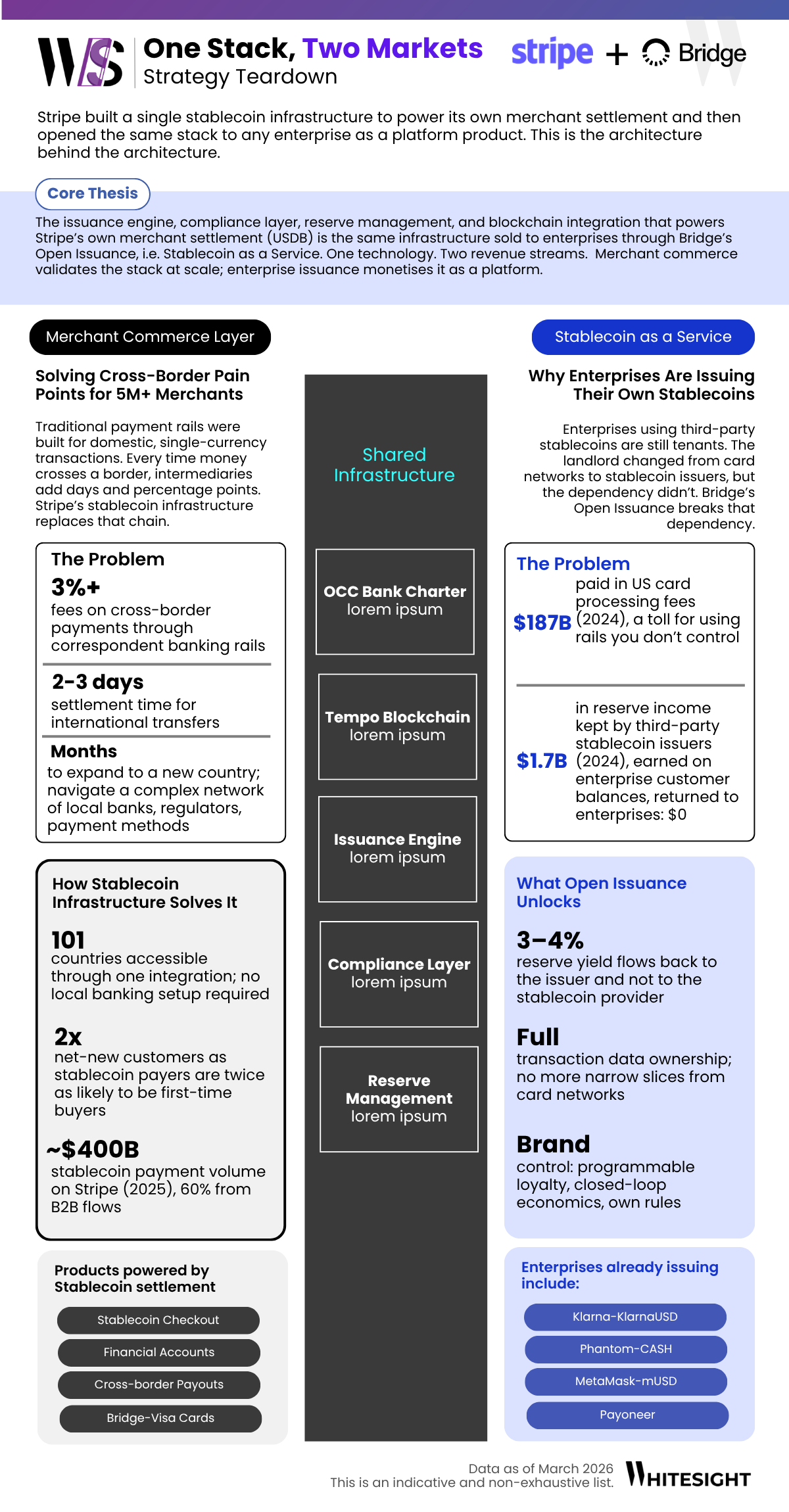

Start at the bottom of the stack. In February 2026, Bridge received a conditional national trust bank charter from the OCC. This gives it federal oversight for stablecoin issuance, digital asset custody, and reserve management. Months earlier, Stripe and Paradigm had launched Tempo, a payments-first blockchain targeting 100,000+ transactions per second with sub-second finality. Tempo raised a $500 million Series A at a $5 billion valuation, with partners including Visa, Deutsche Bank, Nubank, and Revolut. Together, the OCC charter and Tempo provide Stripe with a federally regulated issuance licence sitting on top of purpose-built settlement rails.

One layer up sits issuance. Bridge mints USDB, its own stablecoin backed 1:1 by BlackRock money market funds. But the more consequential product is Open Issuance, launched in September 2025. It lets any company create and manage its own stablecoin with a few lines of code. Reserves are managed by BlackRock, Fidelity, and Superstate. The economic hook is simple: popular stablecoins like USDC and Tether retain all reserve earnings. Open Issuance lets the issuing business capture that yield, currently 3-4% on US Treasuries. For a neobank or fintech sitting on large stablecoin deposits, this changes the unit economics entirely.

Above the issuance sits the products layer. This set of tools moves stablecoins through the three stages of a transaction: collecting them, holding them, and spending them.

On the collect side, Bridge’s fiat-crypto gateway lets businesses accept payments in both traditional currencies and stablecoins through a single integration. Stablecoin acceptance, turned on by default in Stripe’s checkout since September 2025, lets merchants receive stablecoin pay-ins alongside card payments without any additional setup.

Once collected, Stablecoin Financial Accounts, launched in 101 countries, let businesses hold, send, and receive in USDC and USDB. Privy, acquired in June 2025, provides the embedded wallet infrastructure underneath. It powers 110 million+ accounts where users and businesses store their stablecoin balances without managing seed phrases or blockchain complexity.

Then comes spending. Bridge-Visa stablecoin cards convert stablecoin balances to local fiat at the point of sale across 175 million merchant locations. On the payout side, businesses can Stripe to send stablecoins directly to contractors, creators, and suppliers in 69 countries, settling in minutes rather than days.

At the top of the stack sits distribution, the ecosystem of merchants, platforms, and enterprise customers building on this infrastructure. Klarna issued KlarnaUSD for its 114 million customers. Phantom launched CASH for its 20 million+ monthly active users. MetaMask launched mUSD for 100 million+ annual users, spendable at any Mastercard merchant. Payoneer is embedding Bridge-powered stablecoin workflows for nearly 2 million cross-border SMBs. In Latin-America, Felix Pago is using Bridge to power remittances and Starlink is repatriating funds from Argentine sales. Consumers in Nigeria are paying for YouTube Premium and ChatGPT with stablecoins. Airtm provides dollar access in volatile-currency economies, and Chipper Cash handles cross-border payments across Africa.

Then there is Meta. The company that spent years and billions building Libra, only to have regulators kill it, is now experimenting with stablecoin payments. But this time, Meta is not building the infrastructure itself. Zuckerberg has publicly acknowledged that Stripe’s approach ‘makes much more sense than what we were doing.’ Patrick Collison joined Meta’s board shortly after. Bridge is now a reported candidate to provide stablecoin infrastructure for Meta’s apps.

By owning every layer, from the ledger to the license, Stripe has made itself significantly harder to compete against. Pure-play crypto infrastructure providers like Circle or Paxos have built some of these layers, but not all of them. This integration is what separates Stripe from pure-play crypto infrastructure providers.